In China, access to rare earths turns ore into strategic leverage. That leverage now sits in the industrial middle of the chain, where separated oxides are converted into metals, alloys, powders, and high-performance permanent magnets. China produced roughly 69 percent of global rare-earth mine output in 2025. Its control becomes tighter after extraction: the International Energy Agency estimates that China held 91 percent of global refined magnet rare-earth output and 94 percent of permanent magnet production in 2024.[1] The mine is the visible asset. The conversion system is the moat.

The result is a small materials market with large industrial consequences. Rare earth oxides were worth about $6 billion in 2024, and permanent magnets about $25 billion, according to the IMF's April 2026 rare-earth special feature.[2] The IEA estimates that full rare-earth export controls would put $6.5 trillion in annual downstream production at risk outside China, including more than $3 trillion in automotive output and more than $1.5 trillion each in the United States and Europe.[3] A narrow industrial chokepoint can discipline a much larger production system.

Three numbers define the issue. China produced 270,000 metric tons of rare-earth oxides in 2025. The United States produced 51,000 metric tons.[4] U.S. net import reliance for rare-earth compounds and metals rose to 67 percent in 2025, even after domestic mineral concentrate production increased.[5] Diversified projects announced outside China would cover only about half of projected 2035 mining needs, excluding China, 25 percent of refining needs, and well below 20 percent of magnet needs.[6]

The strategic lesson is narrow and uncomfortable. A country can spend years reopening mines and still lack control over the part of the chain that customers actually need. Rare-earth security is measured in qualified magnets, repeatable metallurgical processes, licensed exports, and customer confidence. Ore is the beginning of that system. It is no longer a sufficient proxy for power.

The Conversion Moat

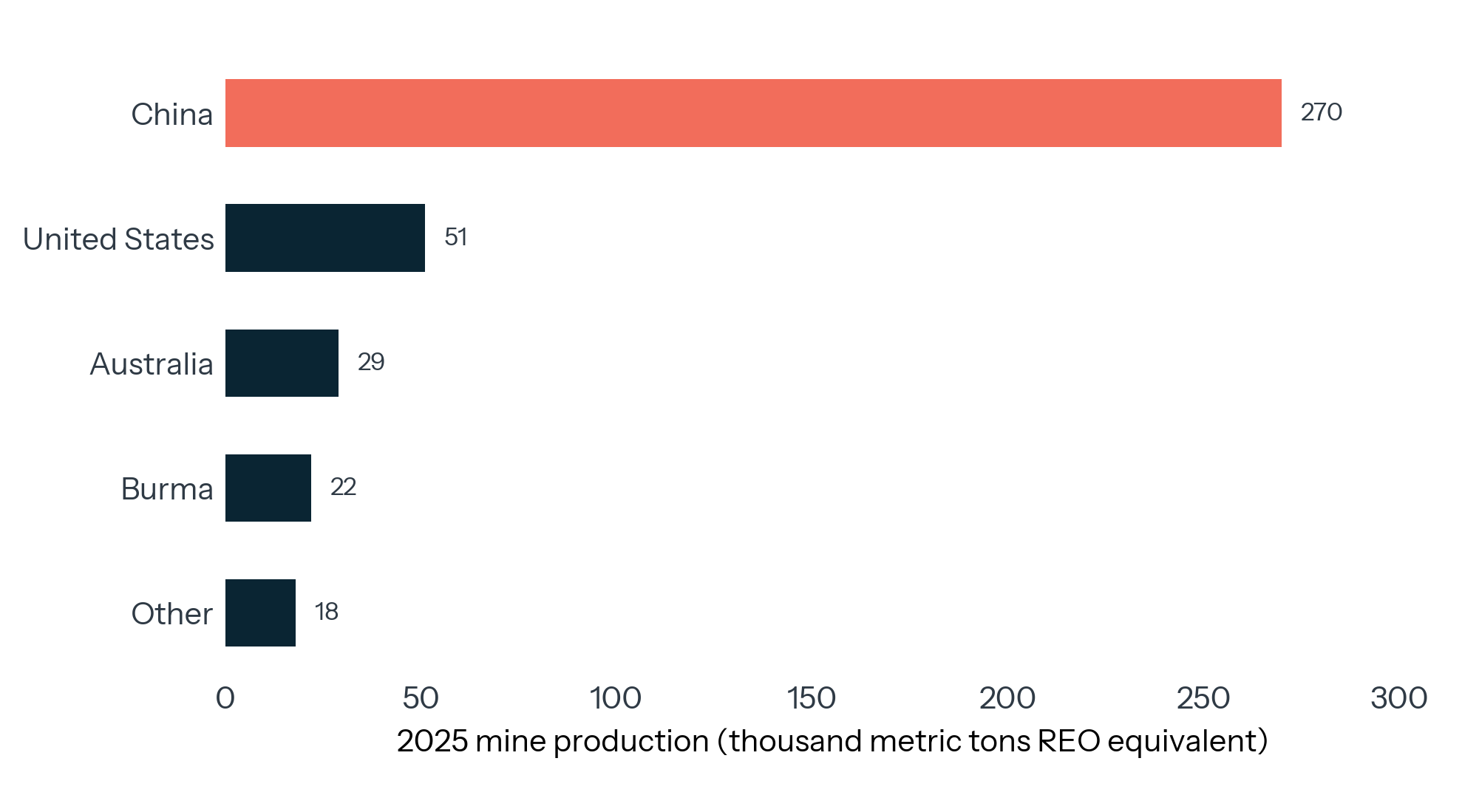

The rare-earth problem has always attracted a geological vocabulary. Reserves, mines, deposits, and resource nationalism are the easiest parts of the story to see. They also create a misleading sense of where leverage sits. In 2025, USGS put world rare-earth mine production at 390,000 metric tons of rare-earth oxide equivalent. China produced 270,000 metric tons, the United States 51,000, Australia 29,000, and Burma 22,000.[7] China is the largest miner by a wide margin. The production base already has more than one pillar.

EXHIBIT 1: The World Has More Than One Mine Base.

China still produced roughly 69% of rare-earth mine output in 2025.

That upstream map misses the material's working form. Rare earths enter motors, missiles, wind turbines, hard drives, industrial robots, and data-center equipment after a long conversion sequence. Ore is mined and concentrated. Mixed rare-earth compounds are separated into individual oxides. Oxides are reduced to metals. Metals become alloys or powders. Those materials are then formed, sintered, magnetized, coated, and qualified into components that buyers can integrate into finished systems. Each step embeds technical knowledge, equipment, environmental tolerance, customer qualification, and production scale.

This is why the Western habit of treating rare earths as a mine race misses the strategic center of gravity. A country can own ore and still depend on Chinese separation. It can separate light rare earths and still lack heavy rare-earth inputs. It can acquire oxides and still lack metallization. It can make magnets and still depend on Chinese alloy feedstock, Chinese equipment, or Chinese-origin intermediate material. The Department of Energy made this point in its 2022 NdFeB magnet supply chain assessment: nearly all stages of the supply chain were concentrated in China, and concentration increased as the chain moved from mining to separation, metal refining, and magnet manufacturing.[8]

Mountain Pass is the cautionary example. The United States has a producing mine. USGS reports 51,000 metric tons of U.S. rare-earth mineral concentrate production in 2025, up from 45,500 metric tons in 2024.[4:1] Yet the same USGS chapter reports that U.S. net import reliance for rare-earth compounds and metals rose to 67 percent of apparent consumption in 2025.[5:1] Domestic ore did not translate automatically into domestic independence. The missing layers were processing, metal, alloy, magnet manufacturing, and customer-qualified delivery.

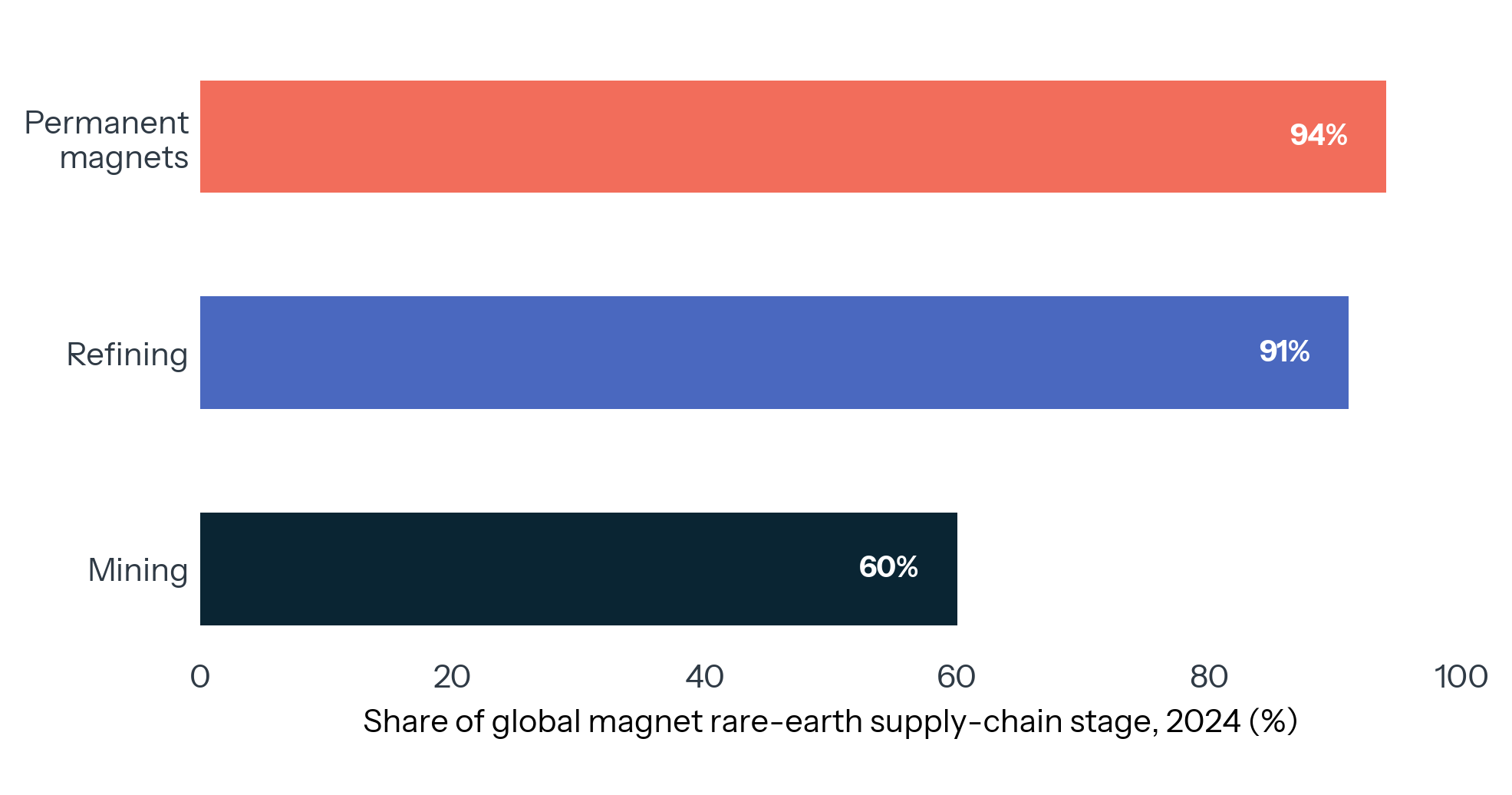

The 2026 data make the same point with a sharper edge. IEA estimates that China held 60 percent of global mined production of magnet rare earths in 2024, 91 percent of refined output, and 94 percent of permanent magnet production.[9] IMF's April 2026 WEO special feature reports a similar shape. China held 88 percent of light-rare-earth oxide separation capacity and 93 percent of light-rare-earth metal refining. For heavy rare earths, China retained 97 percent of oxide separation and 95 percent of metal refining, with permanent magnet production near 90 percent.[10]

EXHIBIT 2: China's Control Deepens After Extraction.

The chokepoint becomes tighter at refining and permanent magnets.

The mine share matters. The downstream share matters more. Mining concentration creates exposure to supply interruption. Processing concentration creates exposure to permission, knowledge, tooling, qualification, and time. A buyer can diversify mined feedstock faster than it can qualify a new high-performance magnet supplier for an automobile platform, an aircraft component, a missile seeker, or a semiconductor tool. The rare-earth chain rewards incumbency. Scale reduces cost. Cost sustains market share. Market share sustains process learning. Process learning sustains the next layer of scale.

China's rock ownership is secondary to its control of the conversion architecture that gives the rock strategic value.

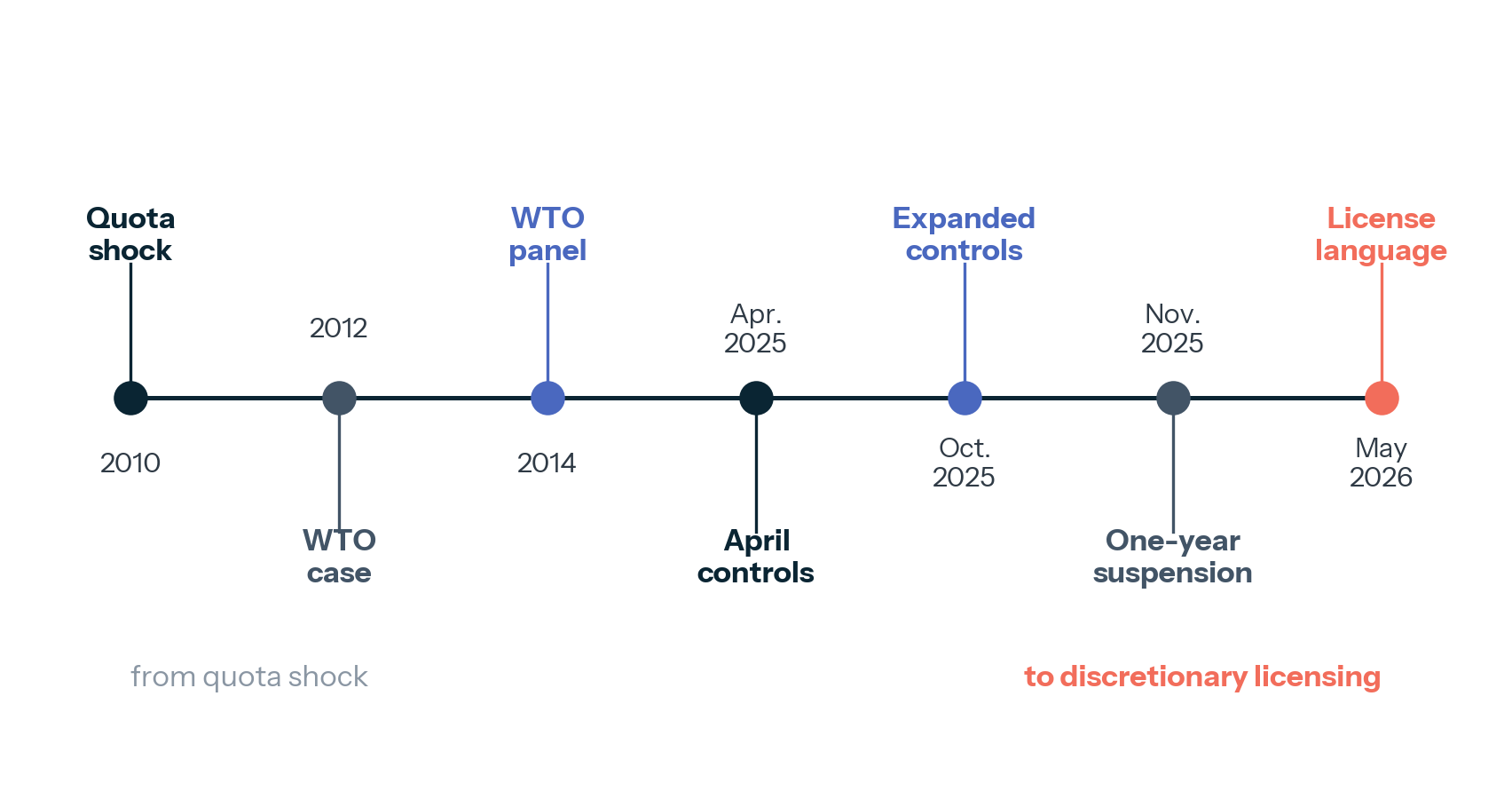

The Quota Lesson

The current magnet chokepoint has history behind it. Rare earths became a strategic issue for Washington, Tokyo, and Brussels in the early 2010s because China imposed export restrictions that exposed the fragility of downstream dependence. The United States, European Union, and Japan initiated WTO action in 2012 after China sharply reduced rare-earth export quotas, creating price spikes and disruption in global rare-earth markets.[11] In March 2014, USTR said a WTO panel found China's export duties, export quotas, and related administration requirements inconsistent with WTO rules.[12]

That dispute mattered because it showed how a materials squeeze can transfer value downstream. USTR's 2014 statement argued that export restraints could raise world prices for raw material inputs while lowering prices for Chinese producers, increasing pressure on foreign downstream producers to move operations, jobs, and technology to China.[13] The legal case addressed quotas and duties. The industrial lesson was broader. A state with sufficient control over a critical input can influence manufacturing location, intermediate-good pricing, and customers' investment behavior.

The 2010 shock also taught buyers the wrong easy lesson. The visible event was an export interruption. The deeper lesson was that market concentration had already allowed one country to become the indispensable swing supplier for a large set of downstream industries. Once a buyer has designed a product around a qualified input, switching becomes a slow engineering project. It is not a spot-market transaction. This is why a short disruption can permanently change procurement behavior.

Japan responded by diversifying. Firms and agencies worked to secure supply from Australia, Malaysia, and other partners. Buyers redesigned some products, reduced heavy rare-earth intensity where possible, and built stocks. That response reduced the narrow vulnerability exposed in 2010. The underlying dependence persisted. The U.S. Commerce Department's published Section 232 report on NdFeB magnets noted that Japan began diversifying away from China in the early 2010s, while the United States, Japan, and Europe remained, to varying degrees, reliant on Chinese inputs.[14]

The persistence matters because Japan was the most serious Western-aligned responder after 2010. It had industrial need, strategic focus, patient capital, and direct experience with disruption. If Japan could reduce exposure without eliminating dependence, the United States and Europe should expect a harder path. A mine can be developed through capital, permitting, and geology. A magnet ecosystem requires a complete chain of materials, equipment, process knowledge, quality control, customers, and production learning.

The old quota era also reshaped China's own strategy. Quotas were visible. They were litigable. They created clear world-price effects and made the policy appear to be an explicit export restriction. After the WTO case, the modern system moved toward a more discretionary and technically framed model. Licensing, end-use review, dual-use classification, customs scrutiny, and customer-specific permissions can slow shipments or redirect confidence without the clean signature of a formal embargo.

China's current system is more precise than the 2010 quota playbook. It can distinguish between civilian and military use, between buyers and countries, between oxides and magnets, and between approved customers and firms stuck in a review queue. It can produce relief in one channel and uncertainty in another. The pressure point becomes administrative time.

The Licensing State

The immediate trigger came on April 4, 2025. China's Ministry of Commerce and General Administration of Customs announced export controls on medium and heavy rare-earth-related items. The controlled list covered samarium, gadolinium, terbium, dysprosium, lutetium, scandium, and yttrium, as well as metals, alloys, targets, oxides, compounds, mixtures, and selected permanent magnet materials.[15] The announcement explicitly included samarium-cobalt permanent magnet materials, terbium-containing NdFeB permanent magnet materials, and dysprosium-containing NdFeB permanent magnet materials.[16]

Those elements are small in tonnage and large in function. Neodymium and praseodymium provide the main magnetic strength in NdFeB magnets. Dysprosium and terbium enhance resistance to demagnetization at elevated temperatures, which is important for traction motors, wind turbines, defense systems, and other demanding applications. Samarium-cobalt magnets are relevant for high-temperature and defense applications. The controlled set, therefore, targeted a narrow band of materials in which substitution incurs performance penalties.

The October 2025 escalation widened the scope. USGS says China expanded rare-earth export controls in October 2025 to include europium, holmium, erbium, thulium, and ytterbium, then suspended the October controls for one year in November. The April controls remained in effect, although China began issuing general export licenses to selected exporters.[17] The suspension reduced near-term pressure while preserving the architecture.

That architecture is visible in the official language. In June 2025, China's commerce ministry said rare-earth-related items have dual-use attributes and that China would review compliant license applications while accounting for civilian demand.[18] On May 20, 2026, after China-U.S. economic and trade consultations, China's commerce ministry reiterated that it reviews compliant, civilian-use license applications for rare earths and other critical minerals.[19] The official message is stability. The operating message is discretion.

EXHIBIT 3: From Quota Shock To Licensing Leverage.

The policy instrument has moved from visible quotas to discretionary approvals.

This distinction matters for firms. A full embargo forces an emergency response. A licensing regime forces a planning response. Buyers ask whether a shipment will clear, whether a supplier's license covers their customer, whether a component contains controlled material, whether a civilian claim will satisfy reviewers, whether a future diplomatic dispute will change the queue, and whether a new product platform can carry that exposure for a decade. The result is a risk premium inside procurement.

The leverage also works through uncertainty. If a magnet maker receives a general license tied to selected customers, those customers gain relief while others remain exposed. If exporters know that military, aerospace, semiconductor, or advanced industrial end uses will attract scrutiny, they will ration attention toward safer accounts. If component makers cannot certify the origin and content of intermediate materials, delays can follow even when the final product has a civilian use. Administrative friction becomes an instrument of industrial policy.

This is why the current rare-earth issue should be read as a capacity-control problem. China holds the physical capacity. It also holds the review mechanism that decides how capacity reaches foreign customers. In commodities, leverage usually comes from withholding volume. In this chain, leverage can come from controlling the terms on which volume becomes reliable.

The timing channel is especially important. An automaker, defense prime, or semiconductor equipment supplier need not believe that every shipment will be blocked. It needs to believe that shipments can become slow, conditional, or politically contingent. That belief changes design choices, inventory policy, supplier qualification, and capital allocation. The licensing state controls exports at the border and changes the expected reliability of the supply chain before the shipment exists.

The Downstream Gap

The Western response is no longer starting from zero. The United States has Mountain Pass mine output. Australia has Lynas and a larger project pipeline. Malaysia, Japan, Estonia, France, the United Kingdom, Vietnam, and others appear in various parts of the separation, refining, and magnet map. The U.S. government has used Defense Production Act authorities, stockpile planning, and supply-chain reviews. Europe has critical raw materials rules and industrial initiatives. Japan has spent more than a decade managing the memory of 2010.

Diversification is uneven. A mine story is easier to finance than a complete magnet chain. Mines have resource estimates, mine plans, reserve statements, and commodity upside. Downstream projects have tougher problems: permitting for chemical separation, high-purity metallurgical know-how, hazardous waste handling, proprietary equipment, qualification cycles, thin margins, and customers who want supply security but resist paying the full security premium before the plant exists.

That last problem is the market failure. A buyer wants the option value of a non-China supplier. It also wants the current price that results from China's scale, subsidies, cluster depth, and lower-cost production ecosystem. A financier wants offtake before backing a refinery or magnet plant. A downstream customer wants proof of output before signing a binding contract. The result is a coordination trap. Everyone can identify the strategic gap, and everyone can wait for someone else to pay to close it.

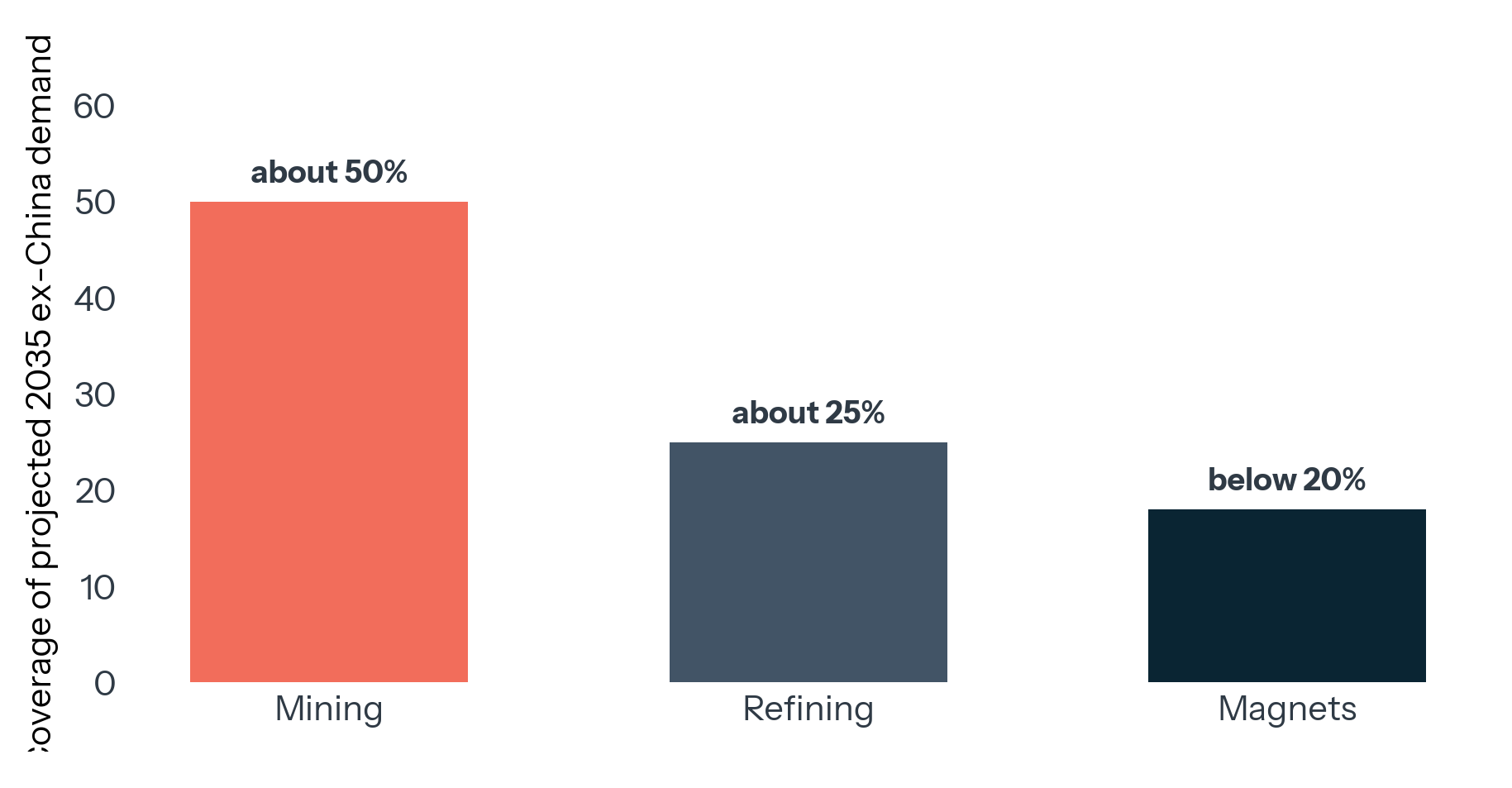

The IEA's 2026 rare-earth report puts numbers on the mismatch. Under current policy settings, demand for magnet rare earths outside China is projected to rise 50 percent by 2035, with the largest contribution coming from EV deployment.[20] Even with planned expansions, expected diversified production would meet only about 50 percent of 2035 mining needs, 25 percent of refining needs, and well below 20 percent of magnet needs.[21]

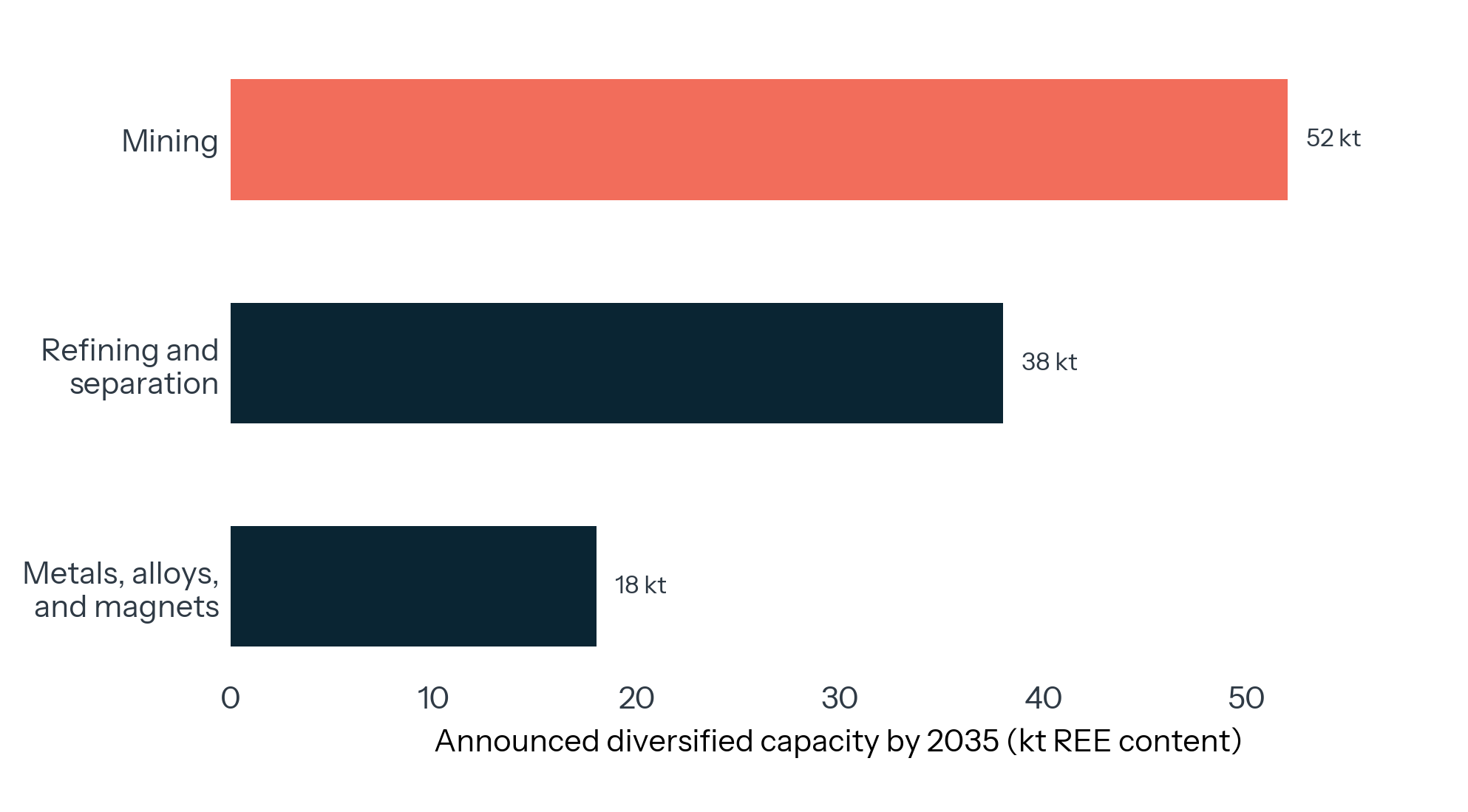

EXHIBIT 4: The Pipeline Thins Downstream.

Announced diversified capacity leaves the largest gap at the magnet stage.

The announced project pipeline has the same downstream thinning. IEA says mining capacity in diversified regions could cross 50 kilotonnes of rare-earth-element content by 2035, led by Australia and the United States with contributions from Brazil, Laos, Tanzania, India, and smaller producers. Refining and separation capacity amounts to below 40 kilotonnes. Metals, alloys, and finished magnets announced as of early 2026 amount to around 18 kilotonnes on a rare-earth-element-content basis, about one-third of diversified mining capacity.[22]

EXHIBIT 5: Mining Projects Outrun Magnet Projects.

Announced projects outside China leave the downstream bottleneck largely intact.

This is the shape problem. A mine-heavy strategy can reduce headline exposure while leaving the decisive bottleneck intact. It can create non-China ore that still needs Chinese or China-linked processing. It can create separated light rare earths while heavy rare-earth inputs remain constrained. It can build a magnet plant that still lacks alloy feedstock, customer qualification, or competitive cost. Supply-chain resilience requires a linked system. The weakest link is downstream.

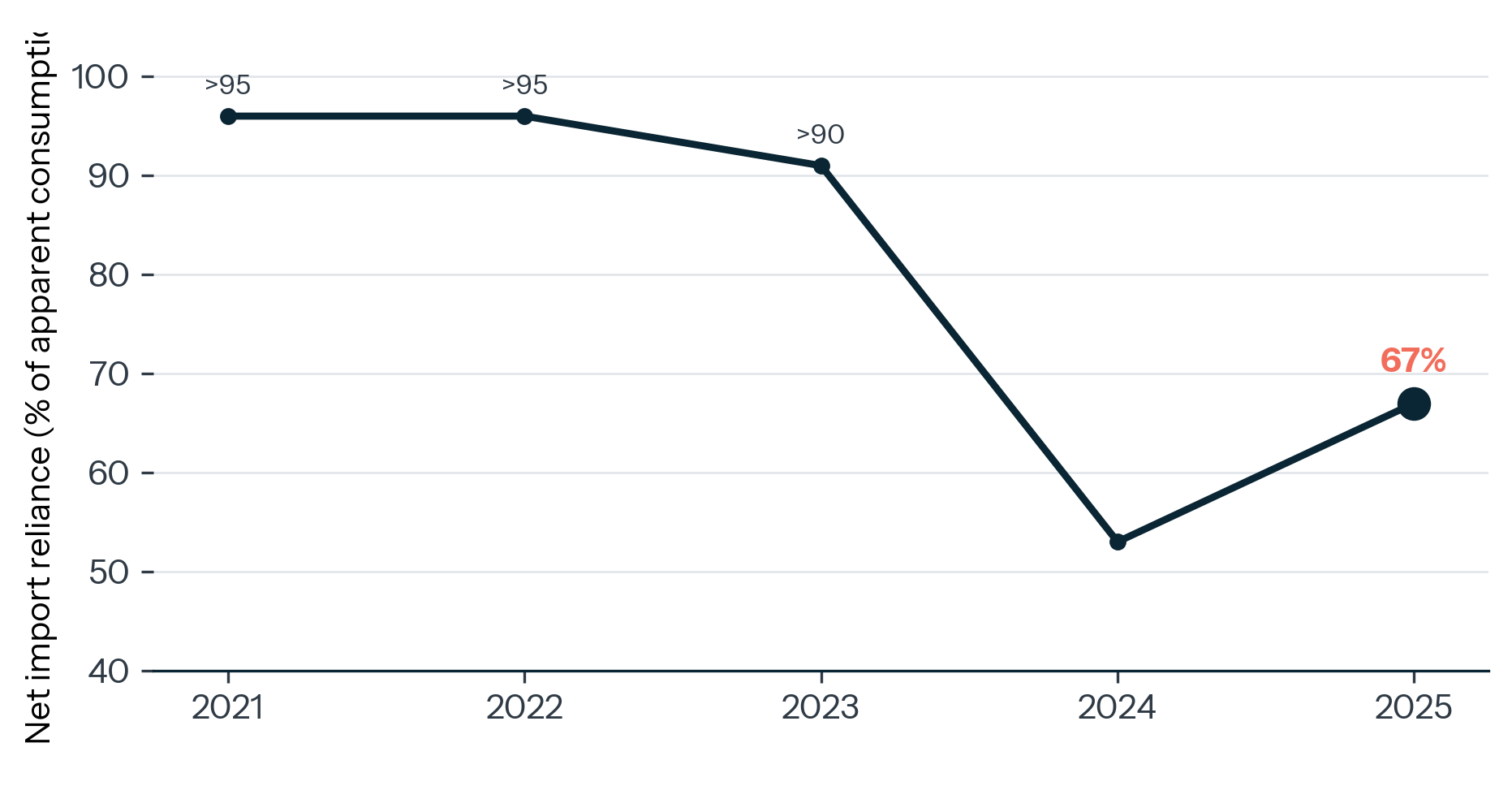

The United States illustrates the point. USGS reports that rare earths were mined and processed domestically in 2025, with 51,000 tons of REO produced in mineral concentrates and 8,900 tons of compounds and metals.[23] U.S. imports of rare-earth compounds and metals increased by 169 percent in 2025, while U.S. apparent consumption of compounds and metals rose to 27,000 tons.[24] Net import reliance for compounds and metals rose to 67 percent of apparent consumption.[25] More upstream activity did not remove refined-product dependence.

EXHIBIT 6: U.S. Dependence Returned In Refined Forms.

Net import reliance for rare-earth compounds and metals rose to 67% in 2025.

The West can make visible progress and remain strategically exposed. Mine production, stockpile purchases, and project announcements matter. Resilience is measured by qualified delivered magnets.

The policy implication is uncomfortable for market purists and industrial-policy maximalists alike. This chain does not need permanent autarky. It does need enough redundant capacity to make coercion less credible. That means bankable demand for higher-cost capacity that may sit partly idle in normal conditions, a result commercial markets rarely provide on their own. The strategic asset is not a subsidized mine. It is a reliable non-China conversion path that buyers can actually use.

The Magnet Multiplier

Permanent magnets are valuable because they convert electricity into motion and motion into electricity with high efficiency and low weight. The DOE's NdFeB assessment calls sintered NdFeB magnets the strongest commercially available magnets and identifies them as key intermediate components in wind turbine generators and electric vehicle traction motors.[26] The same physical logic carries into industrial motors, robotics, precision guidance, actuators, sensors, hard drives, aerospace systems, and parts of semiconductor and data-center equipment.

The magnet is also where the economics become strange. The material input can be small inside a finished product. The component can still determine whether the product meets weight, heat, torque, efficiency, or certification requirements. DOE notes that sintered NdFeB magnets are composed roughly 30 percent rare-earth material, 69 percent iron, and 1 percent boron by weight, and that heavy rare earths such as dysprosium and terbium improve resistance to demagnetization above 120 degrees Celsius.[27] Small additions can be decisive.

This is why substitution is a partial answer. Some applications can use induction motors, ferrite magnets, redesigned drivetrains, reduced heavy-rare-earth loading, or recycled inputs. Those choices are real. They also move the trade-off into efficiency, weight, temperature performance, torque density, cost, and certification. In mass-market consumer goods, those penalties may be tolerable. In high-performance motors, defense systems, robotics, aerospace, and some industrial drives, the penalty can erase the value of substitution.

That creates a leverage multiplier. If a shipment of magnets is delayed, an automaker may lack a motor. If a motor is unavailable, a finished vehicle line can stop. If a defense supplier lacks a qualified high-temperature magnet, redesign is slow because certification, reliability, and performance margins matter. If a semiconductor tool maker faces uncertainty around a controlled material or magnet component, delivery risk propagates into fab schedules. The rare-earth input is small. The production dependency is large.

The IMF's April 2026 rare-earth feature captures that multiplier. It estimates that rare earths are used as inputs in 34 of 405 U.S. sectors, and that those sectors jointly added $233 billion in goods and services value in 2017, or 0.8 percent of nominal GDP.[28] It also estimates that permanent magnets drive about 70 percent of U.S. value added at risk from rare-earth dependence.[29] The magnet is therefore the primary transmission mechanism linking material scarcity to macro-industrial exposure.

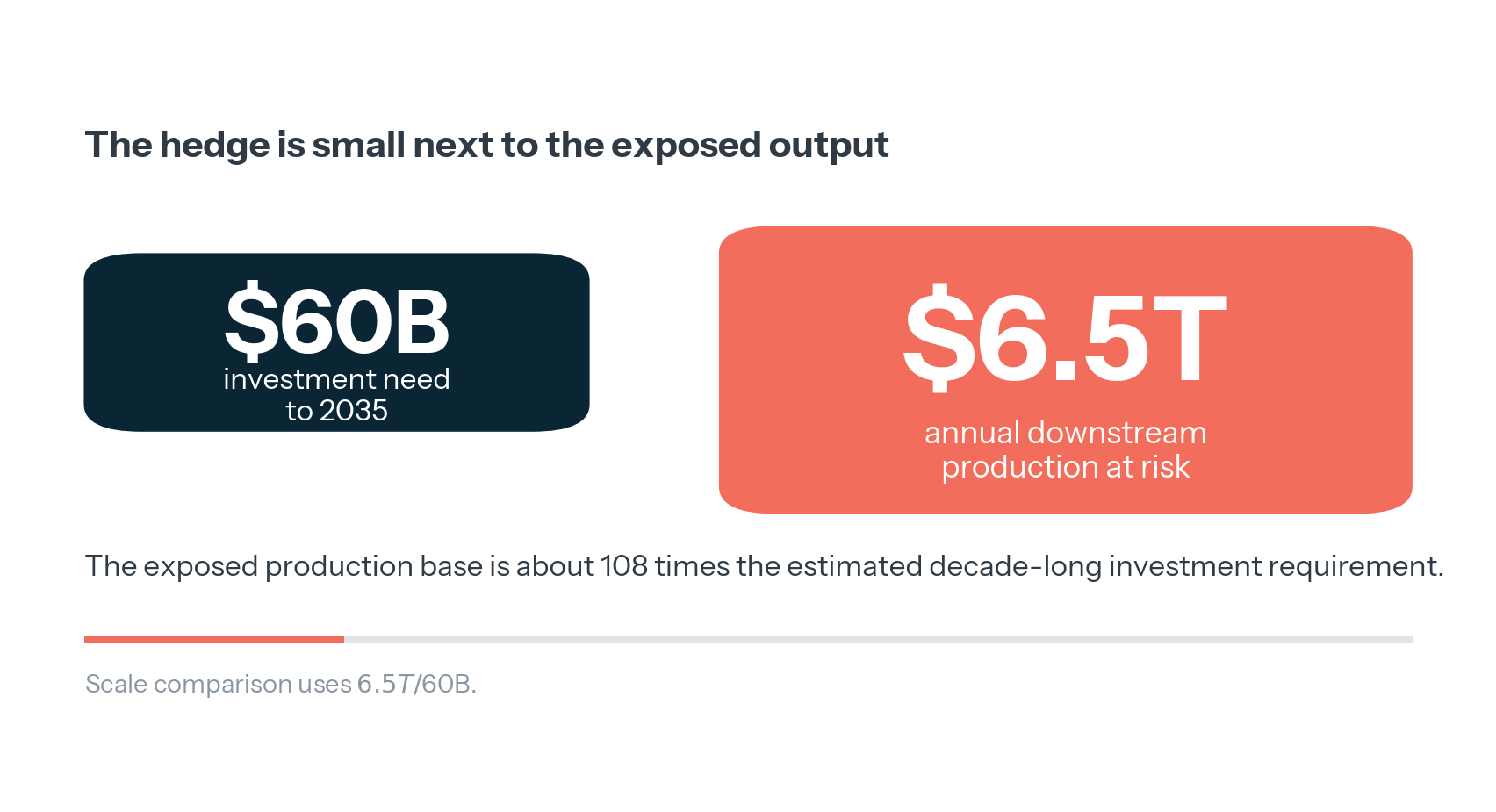

IEA's 2026 estimate is broader and more severe. Full rare-earth export controls would put $6.5 trillion in annual downstream production outside China at risk. Automotive exposure exceeds $3 trillion. The United States and Europe each face more than $1.5 trillion in potential direct losses.[30] These exposure estimates show the size of the production base that depends on a narrow set of materials, processes, and components.

EXHIBIT 7: A Small Market Carries Trillion-Dollar Exposure.

Rare-earth resilience is capital-light compared with the output at risk.

The investment comparison is the cleanest policy signal. IEA estimates that meeting magnet rare-earth demand outside the dominant supplier would require around $60 billion of investment over the next decade. Refining accounts for nearly half of that requirement, and magnet manufacturing around one third.[31] That sum is large for the rare-earth industry. It is small against the output at risk. Coordination is the binding constraint.

Coordination is hard because each participant wants another participant to move first. Miners want offtake. Refiners want feedstock and customers. Magnet makers want alloy supply, equipment, skilled labor, and long-term buyers. Automakers and defense primes want qualified magnets at prices close to Chinese supply. Governments want resilience without permanently underwriting uneconomic capacity. The market equilibrium undersupplies security. China's integrated ecosystem benefits from the opposite structure: scale, domestic demand, supplier networks, lower production costs, and policy tolerance for strategic overcapacity.

Stockpiling helps at the margin. USGS reports that the U.S. FY 2025 potential acquisitions included 300 tons of neodymium-praseodymium oxide, 450 tons of neodymium-iron-boron magnet block, and 60 tons of samarium-cobalt alloy.[32] Stocks can bridge short disruptions. They cannot substitute for live production capacity, qualification, maintenance, recycling, and customer-specific magnet fabrication over a multi-year cycle.

The hard target is an industrial operating base. A resilient chain would have diversified ore sources, sufficient non-China separation for light and heavy rare earths, metal and alloy capacity, magnet plants with qualified customers, recycling that reduces pressure on primary supply, and procurement rules that prevent the system from collapsing whenever Chinese prices fall. The goal is to make China one of several suppliers in the parts of the chain where it is now the system's gatekeeper.

Implications

Defense procurement. Defense systems face the most stringent qualification problem. A civilian motor buyer may sometimes redesign, accept lower efficiency, or switch suppliers over the course of a product cycle. A defense program faces security rules, traceability requirements, reliability standards, and certification timelines. A licensing system that makes heavy rare-earth magnets uncertain can raise cost, slow delivery, and complicate compliance for programs that need high-temperature or high-performance magnets.

Traceability. The immediate procurement task is chain-of-custody discipline. Buyers need to know whether a magnet, alloy, powder, or component contains controlled Chinese material before a crisis begins. This is harder than counting direct imports because exposure can sit several tiers down in motors, actuators, sensors, pumps, drives, or tooling. Firms that cannot map their magnet content will discover the supply chain at the point of delay.

Autos and industrial motors. The automotive sector has the largest direct production exposure in the IEA estimate because rare-earth magnets are used in traction motors, steering systems, sensors, and other components. EV growth will increase demand for rare-earth magnets outside China through 2035. Hybrid systems, industrial drives, and robotics add another layer. Buyers will try to reduce heavy rare-earth intensity and qualify alternative motor designs. The efficiency, weight, and performance penalties will vary by application.

Substitution. Alternative motor designs and lower-heavy-rare-earth magnets are useful hedges. They should be treated as capacity relief. The relevant test is whether a substitute can meet thermal, weight, torque, certification, and cost requirements in the specific system. That answer will differ across consumer electronics, EV platforms, robotics, wind turbines, aircraft, and missiles.

Semiconductor and data-center equipment. Rare earths enter the semiconductor and data-center map through magnets, polishing materials, coatings, motors, drives, and precision systems. The exposure is indirect, which makes it easier to miss. It is also hard to manage because suppliers several tiers down may handle controlled materials. A data-center operator may have no direct rare-earth procurement office, yet still depend on equipment containing magnets and rare-earth-enabled components.

Allied industrial policy. A durable non-China chain will need demand pooling. The investment need is too small to be impossible and too large for fragmented, uncertain demand. The practical solution is a network of offtake agreements, procurement rules, loan guarantees, tax credits, stockpile purchases, and shared qualification standards. The policy target should be downstream capacity, especially refining, metallization, alloys, and magnets. Additional mines help only when they connect to the rest of the chain.

Demand guarantees. The missing instrument is a credible buyer of last resort. Governments can fund mines, but downstream resilience requires customers who will pay for qualified non-China magnets through the cycle. Defense procurement, grid equipment, industrial motors, and public EV fleets can create that demand. Without offtake discipline, new capacity will remain exposed to Chinese price pressure and buyer drift.

China's leverage. Beijing's strongest position is discretionary reliability. It can approve many civilian shipments while still preserving leverage, because customers know approvals can be slow, narrow, or customer-specific. The leverage is strongest where buyers require certified, high-performance parts and cannot switch suppliers quickly. That means China can exercise influence through the shadow of delay, even during periods of partial easing.

The investment test. The IEA's $60 billion figure should be treated as a coordination benchmark. If allied governments and customers cannot mobilize that scale over a decade, they are choosing exposure by default. The figure is smaller than many individual clean-energy, semiconductor, or defense commitments. It is also directed at a chain where the exposed production base is measured in trillions of dollars. The main policy question is whether procurement can create investable certainty before the next supply shock.

The China premium. A resilient chain will usually cost more than the lowest available Chinese supply. That premium is the price of reliability. The question for buyers is whether they pay it gradually through long-term contracts or abruptly through production delays, redesigns, and emergency procurement. A security premium paid before disruption is cheaper than a scramble after licenses slow.

What to Watch

The first marker is the November 2026 expiry of the one-year suspension on China's October 2025 expanded controls. Extension would lower immediate pressure while preserving the system. Expiry would widen the controlled set and test how much inventory and alternative sourcing buyers have built.

The second marker is license behavior. Queue speed, customer coverage, product scope, and renewal terms matter more than broad statements about civilian use. General licenses would reduce acute disruption. Customer-specific approvals would create uneven relief and keep procurement risk high.

The third marker is the distribution of approvals by end use. Civilian labels will matter less than treatment of autos, industrial motors, aerospace, semiconductor tools, data-center equipment, and defense-adjacent suppliers. A licensing system can be permissive in aggregate and restrictive at the frontier.

The fourth marker is heavy rare-earth separation outside China. Light rare-earth mining helps, but dysprosium, terbium, yttrium, and samarium are used in high-temperature magnets and defense-relevant applications. Watch Malaysia, Australia, the United States, Japan, and Europe for separated output backed by shipments and customer qualification.

The fifth marker is alloy and magnet qualification. The useful signal is qualified production delivered into auto, industrial, aerospace, defense, and energy systems. Magnet plants without reliable feedstock and customers are incomplete assets.

The sixth marker is offtake discipline. Long-term contracts from automakers, defense primes, turbine makers, and industrial firms can support non-China capacity. Public resilience language paired with lowest-cost procurement will leave the 2035 downstream gap in place.

The seventh marker is recycling and scrap recovery. Recycling can reduce pressure on sensitive inputs and improve resilience for high-value magnets. The useful evidence is recovered rare-earth content that returns to qualified magnet production.

The final marker is whether governments treat the magnet as the strategic product. Mines are tangible, but the chokepoint sits after the mine. Countries that build capacity in separation, metallization, alloys, powders, and magnets will own resilience. Countries that stop at ore will own a partial hedge.

The bottom line is that the next rare-earth test will likely surface due to licensing friction. The response is operational: map exposure, qualify suppliers, sign bankable offtake, and build midstream capacity before review queues harden.

Notes

- International Energy Agency, "Rare Earth Elements: Pathways to secure and diversified supply chains," published April 8, 2026; IEA executive summary, shares for 2024 magnet rare-earth mining, refining, and permanent magnet production. ↩︎

- International Monetary Fund, World Economic Outlook, April 2026, Commodity Special Feature, "Market Developments and the Economics of Rare Earths," p. 33, rare-earth oxide and permanent magnet market values for 2024. ↩︎

- International Energy Agency, "Rare Earth Elements," executive summary, April 2026, downstream production at risk from full export controls by sector and geography. ↩︎

- U.S. Geological Survey, "Mineral Commodity Summaries 2026," rare-earths chapter, version 1.3, May 2026, world mine production and reserves table. ↩︎ ↩︎

- U.S. Geological Survey, "Mineral Commodity Summaries 2026," rare-earths chapter, U.S. salient statistics, net import reliance for rare-earth compounds and metals. ↩︎ ↩︎

- International Energy Agency, "Rare Earth Elements," executive summary, April 2026, diversified capacity coverage of projected 2035 demand outside China. ↩︎

- U.S. Geological Survey, "Mineral Commodity Summaries 2026," rare-earths chapter, 2025 mine production by country. ↩︎

- U.S. Department of Energy, "Rare Earth Permanent Magnets: Supply Chain Deep Dive Assessment," February 2022, executive summary and supply-chain mapping. ↩︎

- International Energy Agency, "Rare Earth Elements," April 2026. ↩︎

- International Monetary Fund, World Economic Outlook, April 2026, Commodity Special Feature, p. 33 to p. 35, supply-chain stage concentration estimates. ↩︎

- Office of the United States Trade Representative, "United States Wins Victory in Rare Earths Dispute with China," March 26, 2014. ↩︎

- Office of the United States Trade Representative, March 26, 2014, WTO panel findings on export duties, export quotas, and quota administration requirements. ↩︎

- Office of the United States Trade Representative, March 26, 2014, discussion of downstream price effects and pressure to move operations. ↩︎

- U.S. Department of Commerce, "The Effect of Imports of Neodymium-Iron-Boron Permanent Magnets on the National Security," Federal Register publication, February 14, 2023. ↩︎

- Ministry of Commerce and General Administration of Customs of the People's Republic of China, Announcement No. 18 of 2025, April 4, 2025. ↩︎

- Ministry of Commerce and General Administration of Customs of the People's Republic of China, Announcement No. 18 of 2025, controlled permanent magnet materials under samarium, terbium, and dysprosium related items. ↩︎

- U.S. Geological Survey, "Mineral Commodity Summaries 2026," rare-earths chapter, Events, Trends, and Issues. ↩︎

- State Council of the People's Republic of China, "China to enhance review, approval of rare-earth export license applications: commerce ministry," June 12, 2025. ↩︎

- State Council of the People's Republic of China, "China's commerce ministry elaborates on outcomes of China-U.S. economic, trade consultations," May 20, 2026. ↩︎

- International Energy Agency, "Rare Earth Elements," executive summary, April 2026, projected 50 percent increase in outside China magnet rare-earth demand by 2035. ↩︎

- International Energy Agency, "Rare Earth Elements," executive summary, April 2026, projected coverage by diversified capacity. ↩︎

- International Energy Agency, "Rare Earth Elements," executive summary, April 2026, announced diversified mining, refining, and downstream capacity through 2035. ↩︎

- U.S. Geological Survey, "Mineral Commodity Summaries 2026," rare-earths chapter, U.S. domestic production and salient statistics. ↩︎

- U.S. Geological Survey, "Mineral Commodity Summaries 2026," rare-earths chapter, U.S. imports and apparent consumption. ↩︎

- U.S. Geological Survey, "Mineral Commodity Summaries 2026," rare-earths chapter, net import reliance for compounds and metals. ↩︎

- U.S. Department of Energy, "Rare Earth Permanent Magnets: Supply Chain Deep Dive Assessment," February 2022. ↩︎

- U.S. Department of Energy, "Rare Earth Permanent Magnets: Supply Chain Deep Dive Assessment," February 2022, supply-chain overview and magnet composition. ↩︎

- International Monetary Fund, World Economic Outlook, April 2026, Commodity Special Feature, p. 35 to p. 36, U.S. value added at risk estimate. ↩︎

- International Monetary Fund, World Economic Outlook, April 2026, Commodity Special Feature, estimate of permanent magnets' share of U.S. value added at risk. ↩︎

- International Energy Agency, "Rare Earth Elements," executive summary, April 2026. ↩︎

- International Energy Agency, "Rare Earth Elements," executive summary, April 2026, investment requirement to 2035. ↩︎

- U.S. Geological Survey, "Mineral Commodity Summaries 2026," rare-earths chapter, Government Stockpile section. ↩︎