Housing Market Blues

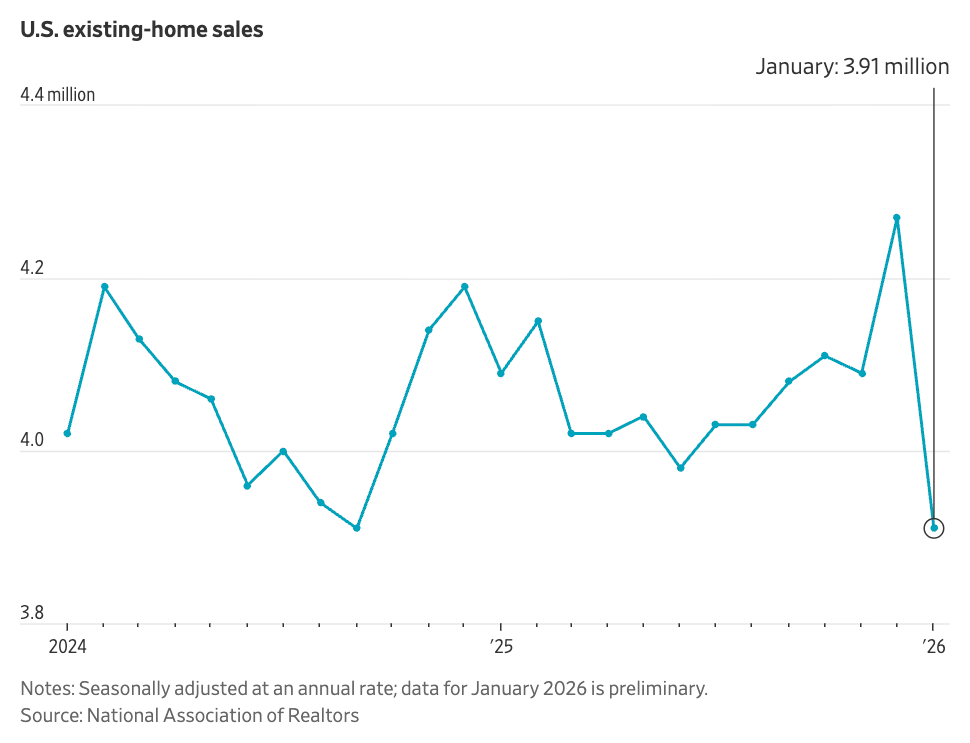

U.S. existing home sales plunged 8.4 percent in January, the sharpest monthly decline since February 2022, even as mortgage rates fell to 18‑month lows. As the Federal Reserve faces unprecedented political pressure, this paradox underscores a troubling reality: lower borrowing costs alone are not enough to revive a housing market constrained by fundamental affordability challenges.

The National Association of Realtors reported existing home sales fell to a seasonally adjusted annual rate of 4.0 million units in January, down from 4.35 million in December. The decline was broad-based, with the West experiencing the sharpest contraction at 7.4 percent despite minimal winter weather disruption – thus undermining explanations that blamed extreme cold for the downturn.

The timing makes the collapse particularly significant. These latest figures reflect contracts signed in November and December, when the average 30-year fixed mortgage rate had dropped to around 6 percent from over 7 percent earlier in 2025. Rather than spurring demand, this one percentage-point decline coincided with mounting market weakness, suggesting deeper structural problems.

The core issue remains affordability. Median home prices reached $396,900 in January, an all-time high for the month and 4.8 percent above year-ago levels.

With mortgage rates still roughly double their pandemic-era lows, monthly housing payments consume a far larger share of household income than historical norms. First-time buyers without existing home equity are, in many cases, effectively priced out of the market.

These affordability pressures persist despite inventory improvements. Available homes increased 17 percent year-over-year to 1.22 million units – yet this represents barely half the typical pre-pandemic supply of 2 million. Homes now take 41 days to sell, the longest for January since 2020, as buyers exercise newfound leverage in negotiations while remaining unable to shift the market overall. The NAR projects a 14 percent sales increase for 2026, but this forecast appears more hopeful than clear-eyed, with other economists predicting just 2 to 9 percent growth.

January’s data confirms that declining mortgage rates have not produced the surge in demand many had anticipated. In the absence of meaningful income growth or substantial price reductions, the housing market is likely to remain stuck in a vicious cycle, preventing both buyers and sellers from achieving their goals.