The Federal Reserve is at a Breaking Point

Jerome Powell's chairmanship ends in May 2026. Before then, a Federal Reserve under unprecedented political assault must decide whether to keep cutting interest rates—or preserve its credibility. The nineteen people around the Federal Open Market Committee (FOMC) table will determine not just borrowing costs, but whether the world's most powerful central bank survives as an independent institution.

A Criminal Indictment Threat Against the Fed Chair

On January 9, 2026, Jerome Powell revealed that the Justice Department had served the Federal Reserve with grand jury subpoenas two days earlier, threatening criminal indictment of the nation's central bank chair. The ostensible issue: Powell's congressional testimony about a multibillion-dollar headquarters renovation running over budget. The real issue, Powell said carefully, was "politically motivated pressure" aimed at influencing monetary policy.

Within hours, central bankers from eleven countries—including the European Central Bank, Bank of England, Bank of Canada, and central banks of Sweden, Denmark, Switzerland, South Korea, Australia, and Brazil—issued an extraordinary joint statement of solidarity. The Financial Times called it "an unprecedented show of support." Republican Senator Thom Tillis announced he would oppose any Federal Reserve nomination "until the legal matter was resolved," warning that "any remaining doubt whether advisers within the Trump Administration are actively pushing to end the independence of the Federal Reserve" should now be gone.

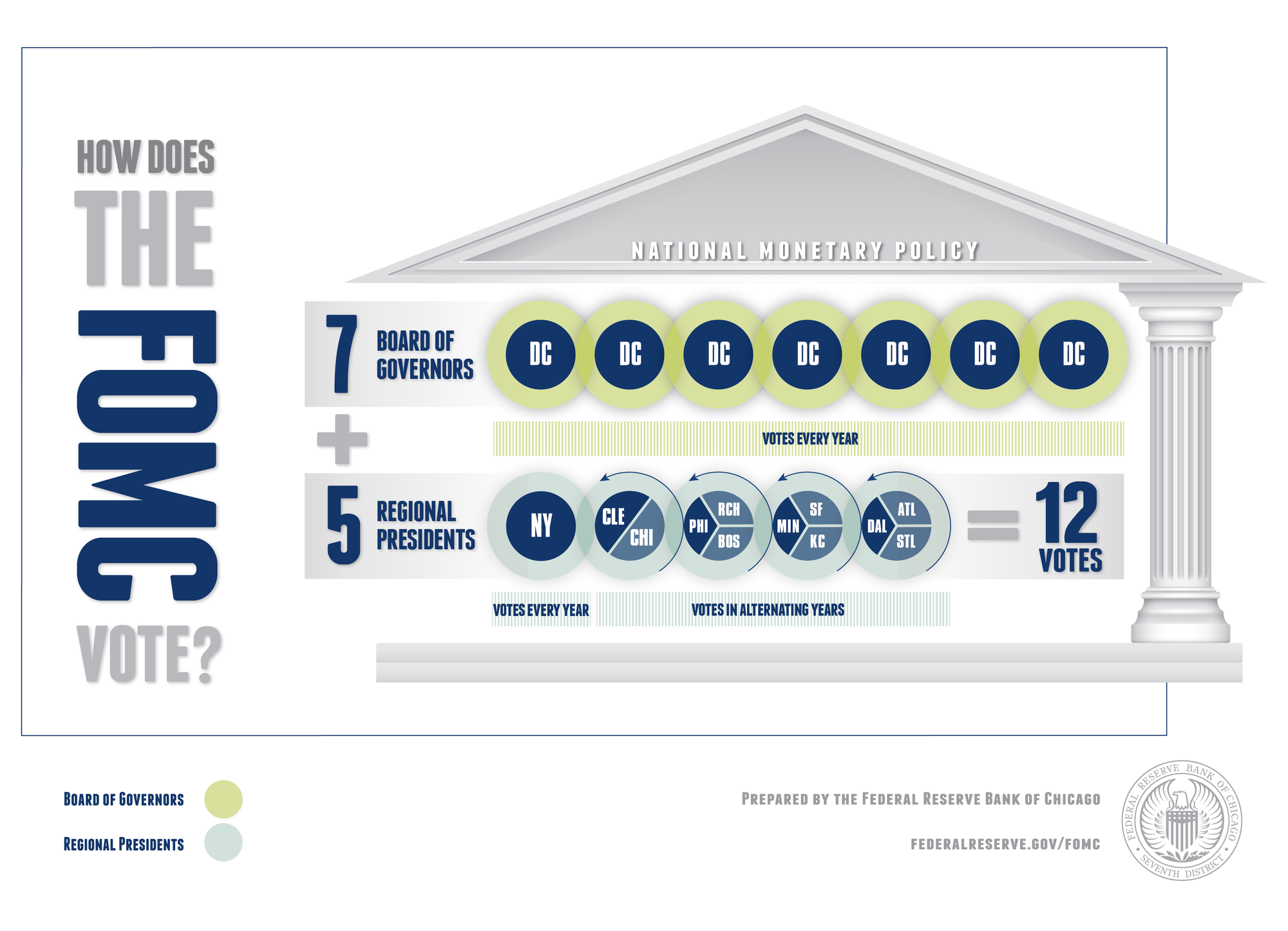

This is the context—crisis—for every monetary policy decision the Federal Open Market Committee makes in 2026. The committee meets eight times per year to set interest rates that determine mortgage costs, business borrowing, credit card rates, and employment prospects for millions of Americans. Twelve members vote—the seven governors appointed by the President plus five rotating regional bank presidents. It's a carefully designed system meant to balance political accountability with technocratic independence. In January 2026, that system is buckling.

Half Here, Half There

No figure better symbolizes the current crisis than Stephen Miran, who joined the Board of Governors on September 16, 2025, while simultaneously serving as President Trump's Chair of the Council of Economic Advisers. He claims to be on "unpaid leave" from the White House. This unholy arrangement—the first time since the 1930s that a Fed official has concurrently held an executive branch position—obliterates the traditional firewall between monetary policy and presidential politics.

Miran is 42, holds a Harvard economics PhD, and worked at Goldman Sachs before joining Treasury during Trump's first term. At a September hearing, he told senators he believed Fed independence "is critical to the well functioning of the economy" while simultaneously refusing to resign his White House position. The Senate confirmed him 48-47 along party lines, with Alaska's Lisa Murkowski the lone Republican voting no. Democrats called it a conflict of interest that could give the president undue influence. Miran's response: he's "very independently minded" and will remain so.

His Fed tenure suggests otherwise. In his four months on the Board, Miran has been aggressively dovish, at Trump's insistence, arguing that "well over 100 basis points of cuts are going to be justified this year" and insisting current policy is "clearly restrictive and holding the economy back." He voted for a half-point cut at his first meeting in September—larger than the quarter-point reduction the committee actually delivered. In a January 2026 Fox Business interview, he claimed inflation is "already running close to the Fed's 2% target once temporary measurement distortions are stripped out" and called for "substantial rate reductions."

Here's what makes this explosive: Miran's term expires January 31, 2026—in two weeks. Trump will either reappoint him for a full fourteen-year term, cementing the White House-Fed connection, or replace him with another loyalist sharing the administration's preference for lower rates. Either way, the boundary between political pressure and monetary independence is being redrawn in real time. Markets are watching. So is every central bank in the world wondering if the Fed's credibility can survive.

Timeline: The Assault on Fed Independence

| Date | Event | Type |

|---|---|---|

| July 2025 | Trump floats firing Powell | 🔴 Political Pressure |

| August 2025 | Trump attempts to fire Lisa Cook; courts block | 🔴 Political Pressure / 🔵 Institutional Resistance |

| September 2, 2025 | Trump nominates Miran to Fed | 🔴 Political Pressure |

| September 15, 2025 | Miran confirmed 48-47 (Senate vote) | 🟡 Key Decision |

| September 16, 2025 | Miran sworn in (day before FOMC meeting) | 🟡 Key Decision |

| December 2025 | Three dissents at FOMC—most since 2019 | 🟡 Key Decision |

| January 9, 2026 | Powell reveals DOJ grand jury subpoenas | 🔴 Political Pressure |

| January 12, 2026 | 11 international central banks issue solidarity statement | 🔵 Institutional Resistance |

| January 27-28, 2026 | First FOMC meeting with new voters | 🟡 Key Decision |

| January 31, 2026 | Miran's term expires | 🟡 Key Decision |

| May 15, 2026 | Powell's Chair term expires | 🟡 Key Decision |

Legend:

- 🔴 Political Pressure - Direct attacks on Fed independence

- 🔵 Institutional Resistance - Fed and allies defending independence

- 🟡 Key Decision Point - Critical moments shaping Fed's future

Leadership Crisis and Legal Limbo

Jerome Powell has chaired the Fed since February 2018 and served as a governor since 2012. His term as Chair expires May 15, 2026. His term as governor runs through January 2028. The question consuming Washington: will he stay on the Board after stepping down as Chair, or depart entirely?

Powell built his career at private equity firm Carlyle Group after serving at Treasury under George H.W. Bush. As Fed Chair, he navigated COVID-19's economic collapse, the fastest inflation surge in forty years, and now the most direct political assault on Fed independence in modern history. Trump has called him a "knucklehead," "numbskull," and "fool," threatened lawsuits over building renovations, and made clear he wants a chair who cuts rates faster. Powell has responded calmly by repeatedly defending the Fed's independence.

The math is simple. If he stays as a governor after May, Powell's vote could check a Trump-appointed chair. If he leaves, the administration gains a board majority.

Heavyweights in Rotation

Philip Jefferson, the Vice Chair, brings stability regardless of who leads. Confirmed in 2023 to a term running through 2036, Jefferson spent decades teaching economics at Swarthmore and Davidson, focusing on poverty and labor markets. His scholarly temperament and long runway provide institutional continuity. Michelle Bowman, elevated to Vice Chair for Supervision in June 2025, came from Kansas banking regulation and represents the community banking perspective Congress mandated. She's emerged as notably hawkish, dissenting in favor of pausing cuts—a sign of growing internal divisions.

Michael Barr resigned as Vice Chair for Supervision in February 2025 after Trump pressure but remains a governor through 2032. His expertise crafting post-2008 financial regulation from the Obama Treasury and University of Michigan Law School continues shaping bank oversight debates. Christopher Waller, a former St. Louis Fed research director with deep technical expertise on balance sheet policy, joined the Board in 2020. He's reportedly on Trump's shortlist to succeed Powell—a choice that would maintain intellectual credibility while installing someone more amenable to rate cuts.

Then there's Lisa Cook, whose fate encapsulates the independence crisis. The Michigan State economist, confirmed in 2022 to a term through 2038, faced a Trump firing attempt in August 2025 over alleged mortgage fraud—charges she vigorously denies. Courts blocked her removal. The case continues. Cook's scholarship on how violence suppressed Black innovation and entrepreneurship makes her a historic appointment. Whether she survives the administration's assault will signal whether the Fed retains any protection from political purges.

Five governors. Two under legal attack. One with simultaneous White House employment. One elevated to reward loyalty. One serving as Vice Chair with a term extending past the next presidential election. This is the leadership team navigating the most politicized environment in Fed history.

The Man in New York

John Williams holds the only permanent regional voting seat. As president of the New York Fed since 2018, Williams executes monetary policy through market operations—buying and selling securities, managing the balance sheet, intervening in financial markets during stress. This critical role, as well as New York's centrality to global finance, requires a permanent policy voice.

Williams spent his entire career in the Federal Reserve System, leading San Francisco before moving to New York. His expertise on the neutral interest rate—the level that neither stimulates nor restrains the economy—makes him pivotal to debates about how much further rates should fall. Unlike governors facing political pressures, Williams answers only to his regional board of directors. He brings Wall Street intelligence directly to FOMC deliberations: what traders are pricing, what credit markets signal, whether policy is transmitting as intended. In a politicized environment, his technical authority and institutional insulation become more valuable.

When Personnel Defy Politics

The regional bank rotation creates a paradox: just as Trump installs dovish governors, the rotating presidents lean hawkish. Four new voters took their seats in January 2026, replacing four who generally supported recent rate cuts despite reservations.

Beth Hammack of Cleveland became Fed president in August 2024 after serving as Goldman Sachs' global treasurer. Her career managing billions in bank liquidity gives her unmatched expertise on how monetary policy transmits through financial markets. But she's called for "maintaining a slightly restrictive policy until convinced inflation is sustainably declining." She worries recent progress could reverse. Markets expecting aggressive easing won't find an ally in Hammack.

Lorie Logan at Dallas is arguably the most technically sophisticated monetary policymaker in the Federal Reserve System. She spent two decades at the New York Fed managing the System Open Market Account—the actual buying and selling of securities that implements FOMC decisions. She oversaw operations during the 2020 COVID crisis, the 2019 repo market disruption, and countless other stress episodes. If anyone understands monetary mechanics, it's Logan. And she's warned that further cuts risk "pushing policy into overly accommodative territory, especially as core services inflation remains stubborn." Translation: we're close to done cutting.

Anna Paulson took over Philadelphia in July 2025 after twenty years at the Chicago Fed, most recently as director of research. She established the Chicago Fed's Insurance Initiative and brings deep financial markets expertise. Early signals suggest she's more moderate than Hammack or Logan, seeing "room for further rate cuts later this year" while maintaining "cautious optimism" on inflation. An economist with a University of Chicago PhD, Paulson may prove the median voter on a divided committee—exactly the position Philadelphia historically occupies.

Neel Kashkari of Minneapolis ran the 2008 TARP bailout at age 35, then reinvented himself as a Fed bank president in 2016. He's been among the committee's more dovish voices historically, favoring aggressive action during downturns. But even Kashkari has expressed "reservations about cutting rates more, noting the resilience of the underlying economy." When the Fed's most dovish regional president sounds cautious, the easing cycle is in trouble.

These four replace Susan Collins (Boston), Austan Goolsbee (Chicago), Alberto Musalem (St. Louis), and Jeffrey Schmid (Kansas City) on FOMC. That outgoing quartet leaned hawkish but supported recent cuts. The incoming quartet is, if anything, more hawkish. The rotation Trump assumed would help his rate-cut agenda may actually block it.

Seven other regional presidents attend every meeting without voting authority. Goolsbee, Obama's former chief economist, has publicly stated he expects more cuts than colleagues—then dissented against December's reduction. Collins of Boston, an international economist and former University of Michigan provost, set a "relatively high" bar for further easing. Schmid of Kansas City, who came from commercial banking, dissented against the last two cuts, insisting "inflation is still too high." Even among non-voters, the consensus tilts toward caution.

What This Means for Your Mortgage, Your Job, Your Wallet

Markets currently price anywhere from one to four quarter-point rate cuts in 2026—an extraordinarily wide range reflecting genuine uncertainty about both economic data and committee composition. The federal funds rate sits at 3.50-3.75% after three cuts in late 2025. Inflation has moderated toward 2.5% but remains above the Fed's 2% target. Unemployment has edged up to 4.2% but remains historically low. GDP growth continues despite recession predictions.

This ambiguous data gives both hawks and doves legitimate grounds for their positions. But here's what households need to understand: the policy outcome now depends less on economic analysis than on political pressure and personnel changes. Consensus is gone.

Consider mortgage rates. The Fed cut rates three times in 2025, yet 30-year mortgage rates have remained stubbornly above 6%. Why? Because mortgage rates reflect long-term expectations, and markets worry about two things: inflation persistence and Fed credibility. If political pressure forces the Fed to cut rates faster than inflation justifies, markets will demand higher long-term yields to compensate for future inflation risk. You could see the perverse outcome of the Fed cutting short-term rates while long-term borrowing costs rise.

The same logic applies to credit card rates, auto loans, and business borrowing costs. If markets lose confidence that the Fed will prioritize inflation control over political demands, the whole yield curve could shift upward—and prices could soar. Businesses facing higher borrowing costs delay expansion and hiring. Consumer spending slows. The very growth Trump demands becomes harder to achieve.

This is why Fed credibility matters. The central bank's power derives from markets believing it will do what it says. That credibility allows the dollar to serve as the global reserve currency, permits the U.S. government to borrow cheaply, and gives monetary policy effectiveness in crises. Lose that credibility, and you lose the tools to manage the next recession.

Credibility or None

FED WITH CREDIBILITY → LOWER BORROWING COSTS

├─ Mortgage rates ↓

├─ Auto loan rates ↓

├─ Credit card rates ↓

├─ Business loan rates ↓

└─ Hiring ↑

FED WITHOUT CREDIBILITY → HIGHER BORROWING COSTS

├─ Mortgage rates ↑ (even as Fed cuts)

├─ Auto loan rates ↑

├─ Credit card rates ↑

├─ Business loan rates ↑

└─ Hiring ↓

Independence on Trial

The January 27-28 FOMC meeting will be the first test of the new voting lineup. Markets expect the committee to hold rates steady—a pause after three consecutive cuts. But the real drama isn't whether they cut; it's whether the committee can maintain any semblance of consensus amid political assault and internal divisions. Don't count on it.

Watch for dissent. In December 2025, three members dissented against the rate cut—the most since 2019. If January brings more dissents, or if the committee splits 6-6 with the Chair breaking the tie, it signals further institutional breakdown. Effective monetary policy requires market confidence that the Fed speaks with one voice. Multiple dissents suggest that confidence is misplaced.

Watch for Powell's public tone. If he responds to questions about political pressure with sharper language, it signals he's preparing to fight publicly for independence. If he's unusually cautious or conciliatory, it suggests he's worried about escalation and trying to de-escalate. Either way, the subtext matters more than the rate decision.

Watch for what happens January 31 when Miran's term expires. If Trump reappoints him for fourteen years, it cements the White House-Fed connection as the new normal. If Trump appoints someone else, the question becomes: is that person even more dovish, or does the administration recognize Miran's presence has become counterproductive?

And watch for May Madness, when Powell's chairmanship expires. Names circulating as potential successors include Kevin Hassett (Trump's National Economic Council director and a rate-cut advocate), Kevin Warsh (a former Fed governor who favors tighter policy), and Christopher Waller (the current governor who could maintain credibility while being more amenable to cuts). Each choice sends a different signal about how far Trump will push.

The Choice Before the Committee

The nineteen people currently participating in FOMC meetings have formidable resumes: Harvard and University of Chicago PhDs, decades of central banking experience, crisis management expertise, scholarly distinction, Wall Street mastery. Powell graduated from Princeton and Georgetown Law. Jefferson published groundbreaking research on labor markets. Hammack managed Goldman's global treasury. Logan executed monetary policy during the worst financial crisis since the Depression. Paulson established an entire research initiative on insurance regulation. These aren't political hacks or ideologues. They're serious policymakers.

But credentials won't matter if political pressure determines outcomes. The Fed's design—governors serving at presidential pleasure, regional presidents insulated from Washington, staggered terms preventing any president from remaking the committee—was meant to balance accountability with independence. That design is being stress tested before our eyes.

One path preserves independence through institutional resistance: Powell potentially staying on as governor to maintain a check, regional presidents using their votes to prevent politically motivated easing, courts protecting Cook from arbitrary firing, and public pressure from international allies defending Fed credibility. This path requires the committee to accept political attacks, market volatility, and presidential fury as the price of long-term institutional survival.

The other path subordinates monetary policy to political demands: cutting rates to satisfy Trump regardless of inflation risks, allowing White House officials to simultaneously serve on the Board, and accepting that Fed appointments reward loyalty over expertise. This path provides short-term accommodation and presidential approval at the cost of long-term credibility and effectiveness.

The choice isn't between hawks and doves, or between fighting inflation and supporting employment. It's between an independent central bank that makes unpopular decisions when necessary, and a politicized one that serves whoever holds the White House. Markets are watching. The world is watching. And nineteen people in Washington will make the choice that determines which Federal Reserve emerges from 2026—the credible technocratic institution that has anchored American prosperity, or a compromised tool of presidential abuse.

The stakes are that high. The crisis is that real. And the clock is ticking toward May 15.