The Federal Reserve's Split Personality

The Federal Reserve doesn't look like a central bank. The Bank of England runs from Threadneedle Street. The ECB commands from Frankfurt. The Bank of Japan sits in Tokyo.

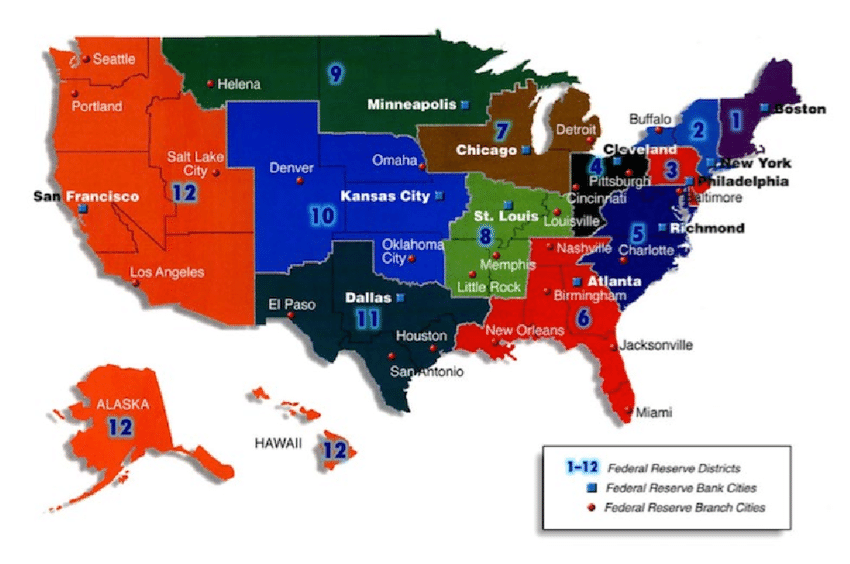

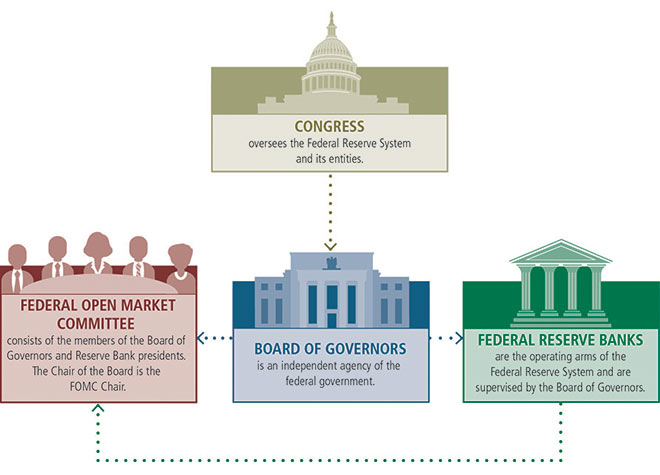

The Federal Reserve sprawls across thirteen cities with power deliberately fragmented between Washington and twelve regional banks—Boston, New York, Philadelphia, Cleveland, Richmond, Atlanta, Chicago, St. Louis, Minneapolis, Kansas City, Dallas, San Francisco.

This fragmentation is not bureaucratic inefficiency. It is a deliberate constitutional defense against political capture of monetary power. This isn’t by accident. The Federal Reserve’s architecture is designed to prevent concentrated financial power from controlling the nation’s money.

That design is being stress-tested right now—not for the first time, nor by the first or last president who will try.

Panic, Power, and Design

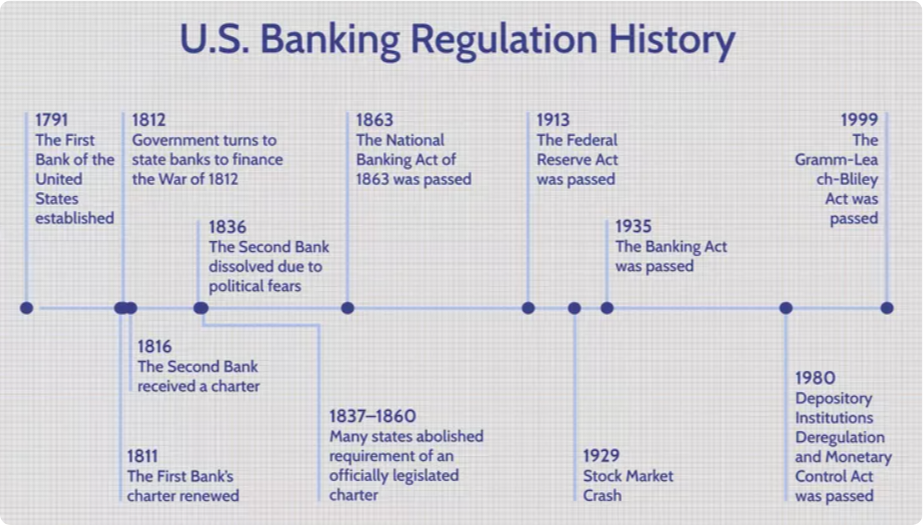

September 1907. Failed copper market speculation triggers bank runs in New York. Stock values at the New York Exchange plunge nearly 50 percent. The financial system edges toward collapse.

No government institution can respond. No central bank exists. The United States relies instead on J.P. Morgan—private citizen, finance mogul—to personally organize lines of credit and stabilize the banking system.

Morgan succeeds. But the lesson is unmistakable: the world's largest industrial economy cannot continue depending on wealthy individuals to prevent financial catastrophe.

Congress spent six years fighting over how to address the financial system's shortcomings. Republicans wanted a single powerful central bank. Democrats demanded multiple independent regional banks tailored to local conditions. Both plans gave private bankers control over leadership selection.

The political breakthrough came after the 1912 elections swept Democrats into the White House and Congress. President Woodrow Wilson pushed a compromise drafted by Congressman Carter Glass of Virginia and Senator Robert Owen of Oklahoma.

Glass wanted maximum decentralization—as many as twenty regional banks with minimal Washington oversight. Owen insisted on government control. Wilson demanded both: regional structure and centralized supervision.

What emerged was the Federal Reserve Act of 1913. Eight to twelve regional Reserve Banks, each with its own board of directors drawn from banking and business. A Federal Reserve Board in Washington composed entirely of presidential appointees to provide oversight. A Federal Advisory Council of twelve bankers elected by regional banks to voice industry concerns.

The compromise deliberately left key power relationships undefined. Who controlled monetary policy—Washington or the regional banks? The law didn't specify. How much independence would regional banks exercise? Intentionally vague.

These omissions were not poor writing. They were political necessities. The only way to pass central banking legislation was to allow competing factions to interpret the law differently.

Wilson signed the Federal Reserve Act on December 23, 1913. He later told reporters:

We have purposely scattered the regional reserve banks and shall be intensely disappointed if they do not exercise a very large measure of independence.

They did. For twenty years, regional banks operated with substantial autonomy. The Federal Reserve Bank of New York, led by Benjamin Strong from 1914 to 1928, dominated monetary policy through sheer force of Strong's personality and New York's position in financial markets. Washington provided general supervision. Real power resided in the districts.

The Great Depression Changes Everything

The 1929 crash exposed fatal flaws in decentralized control. Regional banks pursued inconsistent policies. Some tightened credit during contraction. Others maintained looser standards. The money supply collapsed. Banks failed by the thousands.

By 1934, Marriner Eccles—Utah banker turned Treasury official—had seen enough. President Franklin Roosevelt appointed him governor of the Federal Reserve Board with a mandate: fix the system.

Eccles drafted legislation to centralize power in Washington. Senator Carter Glass—architect of the original 1913 decentralized system—led opposition. Glass rewrote major sections. But the core survived.

The Banking Act of 1935 created the Board of Governors—seven presidential appointees serving fourteen-year terms. It removed the Treasury Secretary and Comptroller of the Currency, ending direct executive branch presence. Most critically, it created the Federal Open Market Committee (FOMC) in its modern form, centralizing control over open market operations that individual regional banks had previously conducted independently.

The new FOMC consisted of the seven-member Board of Governors plus five regional bank presidents. New York held a permanent seat. The other eleven rotated through four positions. This gave Washington majority control while preserving regional representation.

Glass lost the fight but saved the regional banks' voting rights. The Fed emerged far more centralized than the 1913 design—but not fully centralized. Regional banks retained FOMC votes, research capacity, supervision authority, and boards selecting bank presidents subject to Board approval.

The result was neither a European-style central bank nor the loose federation Glass envisioned—but a hybrid designed to fail slowly rather than collapse suddenly.

The New York Exception

Among the twelve regional banks, New York occupies special status. It conducts open market operations for the entire system, maintains foreign central bank relationships, and sits in global finance's heart with direct market access. The New York Fed's president participates in every FOMC meeting with permanent voting rights—the only regional president with this privilege.

During the 2008 crisis and 2020 pandemic, New York functioned as de facto headquarters, creating tension with a system designed to prevent regional dominance. Defenders argued necessity—open market operations require constant securities market engagement concentrated in New York. Critics saw Eastern financial dominance with a different organizational chart.

Intelligence at Scale

Regional banks systematically collect geographically dispersed economic intelligence. When Atlanta contacts report labor shortages while San Francisco describes technology layoffs, policymakers learn whether national unemployment figures reflect universal conditions or regional variance.

For attentive observers, these regional divergences often matter more than headline CPI or payroll prints. These differences flow into policy through the Beige Book—narrative evidence supplementing quantitative data published before each FOMC meeting. The system enables specialized research. Kansas City develops agricultural economics expertise. Dallas focuses on energy. Minneapolis pioneers Native American economic development work.

Centralized central banks must approximate this. The Fed builds it into structure.

The Enduring Tension

One interest rate serves the entire country. The FOMC cannot set different rates for booming technology centers versus struggling manufacturing regions. Regional perspectives inform national decisions but cannot produce differentiated policies.

This becomes acute when different parts of the country experience dramatically different conditions. During the 2010s recovery, coastal metros rebounded fast while Midwest manufacturing stagnated. The single national rate addressed neither adequately. The constraint is real. The benefit is institutional resilience against political pressure campaigns.

The Federal Reserve's organizational architecture isn't about administrative efficiency. It's about institutional durability under political pressure.

Three implications matter for investors and policymakers:

First, expect monetary policy independence to remain contested but resilient. The 1913 compromise created geographic distribution of power. The 1935 Banking Act centralized control while preserving regional voting rights. Both built structural defenses against political pressure.

Second, watch regional bank research and Beige Book data for early signals on economic divergence. Regional intelligence spots inflection points before national aggregates. Eccles centralized monetary policy but channeled regional knowledge into decision-making rather than eliminating it.

Third, understand that Fed governance fights determine whether the United States maintains an independent central bank capable of making economically optimal but politically unpopular decisions. Glass and Eccles fought bitterly in 1935 over centralization. Glass lost most battles but won the war that mattered: regional banks retained FOMC votes.

Modern Challenges

The Fed's distributed structure matters most when political pressure hits the institution. President Trump's Justice Department just served Fed Chair Jerome Powell with criminal investigation subpoenas—ostensibly about headquarters renovation costs, actually about interest rate policy.

Powell's January 12, 2026 response was unprecedented. He publicly called the investigation a "pretext" designed to force rate cuts through "political pressure or intimidation." He's defending institutional independence, not personal reputation.

Structure matters here. Even if Trump replaces Powell when his term expires in May, he faces eleven regional bank presidents reappointed in December 2025 with terms running to 2031. These presidents vote on the FOMC. They answer to regional boards, not Washington. The President cannot fire them.

The 1913 compromise—refined but not eliminated by the 1935 Banking Act—anticipated exactly this scenario. Geographic distribution of authority creates friction, slows political capture, forces compromise.

The system Carter Glass fought to preserve in 1935 is doing precisely what he intended: making it difficult for any single power center—including the White House—to control monetary policy.

The structure endures because both reforms preserved enough distributed authority to prevent capture. The Fed's split personality—Washington headquarters, regional banks, shared power—makes it harder to bend monetary policy to political will.

Eighty-five years after Eccles centralized control, the architecture he created while fighting Glass is protecting the institution from exactly the political pressure both men feared most. Any reform that simplifies the Fed’s structure will almost certainly weaken its independence—and history suggests the price of that mistake is paid during the next crisis, not the next election.