Capital is King

Analyzing three decades of foreign direct investment

A short intelligence memo on Capital Markets. Read for the core judgment, evidence trail, and decision implication.

Analyzing three decades of foreign direct investment

- Frame

- Briefing

- Topic

- Capital Markets

- Access

- Free

While most economic data measures past decisions, foreign direct investment (FDI) is forward-facing by definition. When a firm builds a factory, acquires a company, or establishes lasting operations abroad, it is committing capital that cannot be easily reversed.

That commitment reflects many considerations at once: the size and growth of the market, the cost of labor, the quality of infrastructure, the reliability of contracts and courts, the tax environment, and increasingly, the geopolitical alignment of the host country with the investor's home country. When FDI flows shift, it is usually because one or more of those factors has changed in a meaningful way.

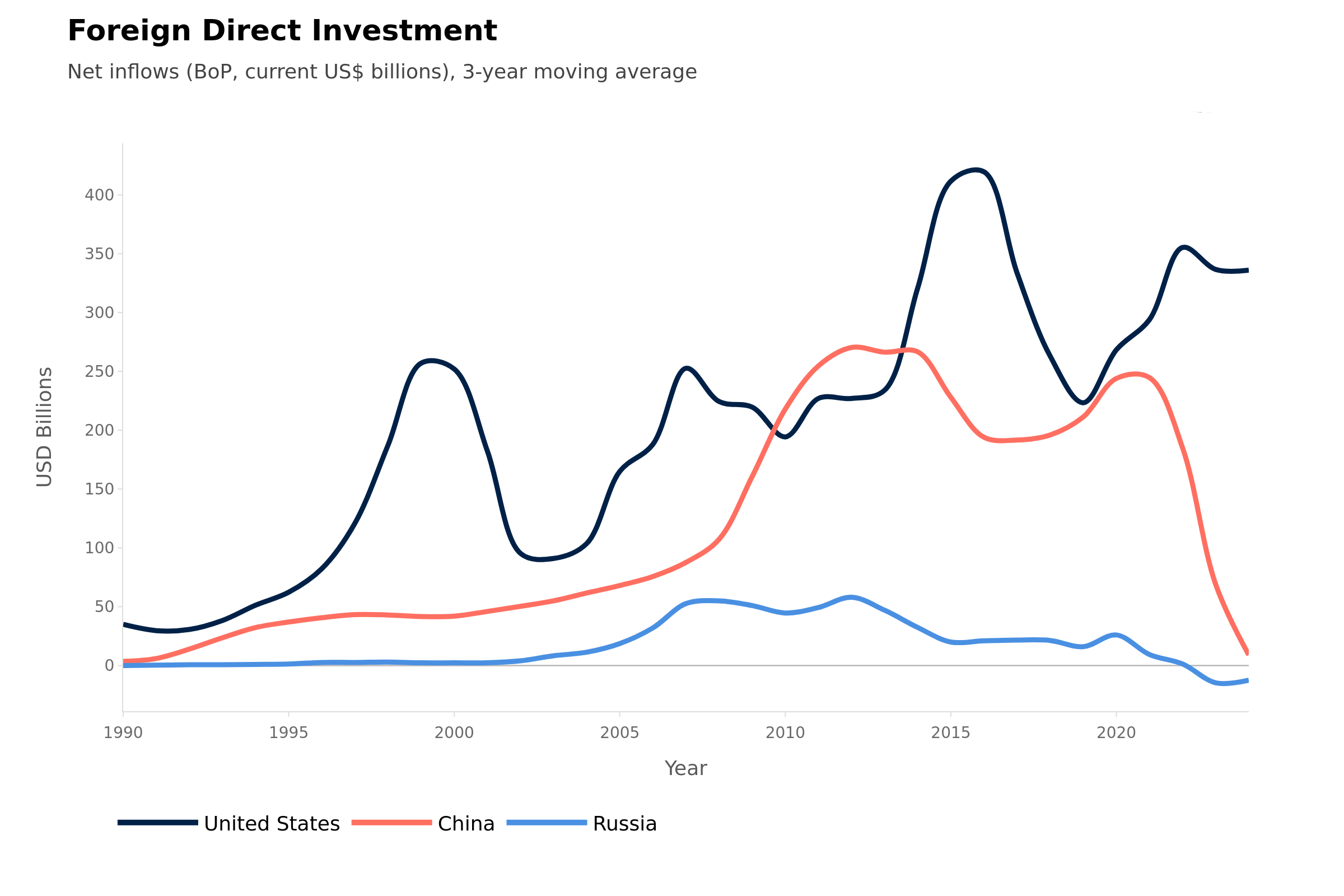

The chart below tracks net FDI inflows into the United States, China, and Russia from 1990 to the present, using a three-year moving average to surface long-run trends rather than single-year noise. The U.S. lead is more fragile than it appears, China's investment model has broken down structurally, and Russia has exited the FDI system entirely. Together, these three trajectories define the terms on which capital will move for the next decade.

America's Lead is Fragile

The U.S. curve moves in significant waves, and the waves matter. The late 1990s surge was driven by a boom in cross-border mergers and acquisitions, fueled by internet-era optimism and broad deregulation. By 2000, the U.S. was absorbing roughly $300 billion annually. The dot-com collapse took flows with it. They recovered through the mid-2000s, then dropped again in the financial crisis.

The mid-2010s brought another surge, reaching roughly $400 billion, driven largely by pharmaceutical and technology sector deals and a wave of corporate inversions before tax reform closed those loopholes. More recently, the CHIPS Act and Inflation Reduction Act introduced something new: explicit industrial policy designed to actively reshore manufacturing investments to the United States.

That policy turn is significant because it signals a quiet admission. Left purely to market logic, capital does not automatically favor the United States over lower-cost alternatives. The country's structural advantages (deep capital markets, a large consumer base, strong legal protections, dollar reserve status) remain durable, but they are no longer sufficient on their own to dominate an increasingly competitive market for foreign investment. The U.S. is now actively competing for capital, a posture it did not need for most of the postwar period. The lead has endured. The terms on which it endures have changed.

China's Bet Unwinds

China's FDI trajectory is the most consequential shift in the data. FDI inflows were negligible in the early 1990s, as the country remained largely closed to foreign ownership. WTO accession in 2001 was the decisive turning point. Multinationals directed massive capital investments into low-cost manufacturing, vast logistical infrastructure, and a rapidly growing consumer market. By the early 2010s, China was absorbing over $250 billion annually, nearly on par with the United States.

The peak came between 2013 and 2015, after which FDI plateaued and then declined. Three forces drove that shift. Chinese labor costs had risen significantly over two decades of growth, eroding the wage advantage that had originally anchored the investment case. The U.S.-China trade war, beginning in 2018, introduced tariff and policy risk that firms had never previously needed to price in. The pandemic then accelerated corporate adoption of "China Plus One" strategies, in which companies retained some China operations but built parallel capacity in Vietnam, India, Mexico, and elsewhere to reduce single-country concentration.

By 2022-2023, net FDI flows into China turned negative for the first time in decades. Outgoing capital exceeded incoming capital, meaning foreign firms were actively withdrawing commitments they had already made. The implication is structural and far-reaching. The model that made China the defining FDI story of the last thirty years (cheap labor, open access, export-driven growth) has run its course. What replaces it, if anything does, is anyone's guess.

Russian FDI is Dead

Russia's curve is smaller in absolute terms, reflecting the broader limits of foreign capital. Flows were negligible throughout the 1990s, a decade defined by institutional chaos, hyperinflation, and uncertain property rights. The commodity boom of the 2000s seemed to reflect a new Russia. As oil prices rose and macroeconomic conditions stabilized, multinationals moved to access Russia's energy and natural resource base. FDI inflows peaked around 2013.

The 2014 annexation of Crimea fractured that confidence. Western sanctions reduced Russia's access to foreign capital, prompting firms to reassess their exposure. FDI dropped sharply from there. The 2022 invasion of Ukraine ended the story entirely. A coordinated Western sanctions regime, combined with corporate exits en masse, pushed net FDI into the red. Capital was withdrawn, written off, or lost to forced divestiture.

Russia is now, in investment terms, an isolated economy. That isolation will likely outlast the war in Ukraine. The legal and reputational risk of operating in Russia has been priced into corporate decision-making in a way that will not reset quickly, regardless of how and when Putin's war ends.

The Reallocation

Capital flows are being reorganized around resilience and geopolitical alignment. Firms that once optimized for cost or market access are now pricing in sanctions exposure, supply chain concentration, and the legal reliability of the host country. That repricing is clear in the data, and the trend is accelerating.

The early beneficiaries are visible. Vietnam and India are absorbing manufacturing capacity diverted from China. Mexico is gaining from nearshoring strategies tied to U.S. market access. The Gulf states are converting sovereign wealth into inbound investment infrastructure. None of these destinations yet operates at the scale or institutional depth of the U.S. or pre-2015 China, but the diversification is structural, and the capital is moving.

The U.S. still leads, and it is increasingly using government policy to sustain that position. China remains a large economy, but the frictionless investment relationship that defined 2001-2015 is over. Russia has exited the system.

The world that emerges from this reallocation is one where capital concentrates in fewer places, on more conditional terms, with geopolitical risk underwriting every major allocation decision. That world will be more resilient to the kind of single-country shocks that the Russia crisis exposed. It will also be less efficient, with higher costs and more redundancy built into global supply chains as the price of that resilience. For firms and governments competing for capital, the implication is direct: the investment case now requires geopolitical credibility as a prerequisite, and countries that cannot offer it will find themselves excluded from the flows that compound growth over time.