The Most Profitable Business Ever Built

How Alphabet stands apart

A short intelligence memo on Capital Markets. Read for the core judgment, evidence trail, and decision implication.

How Alphabet stands apart

- Frame

- Briefing

- Topic

- Capital Markets

- Access

- Free

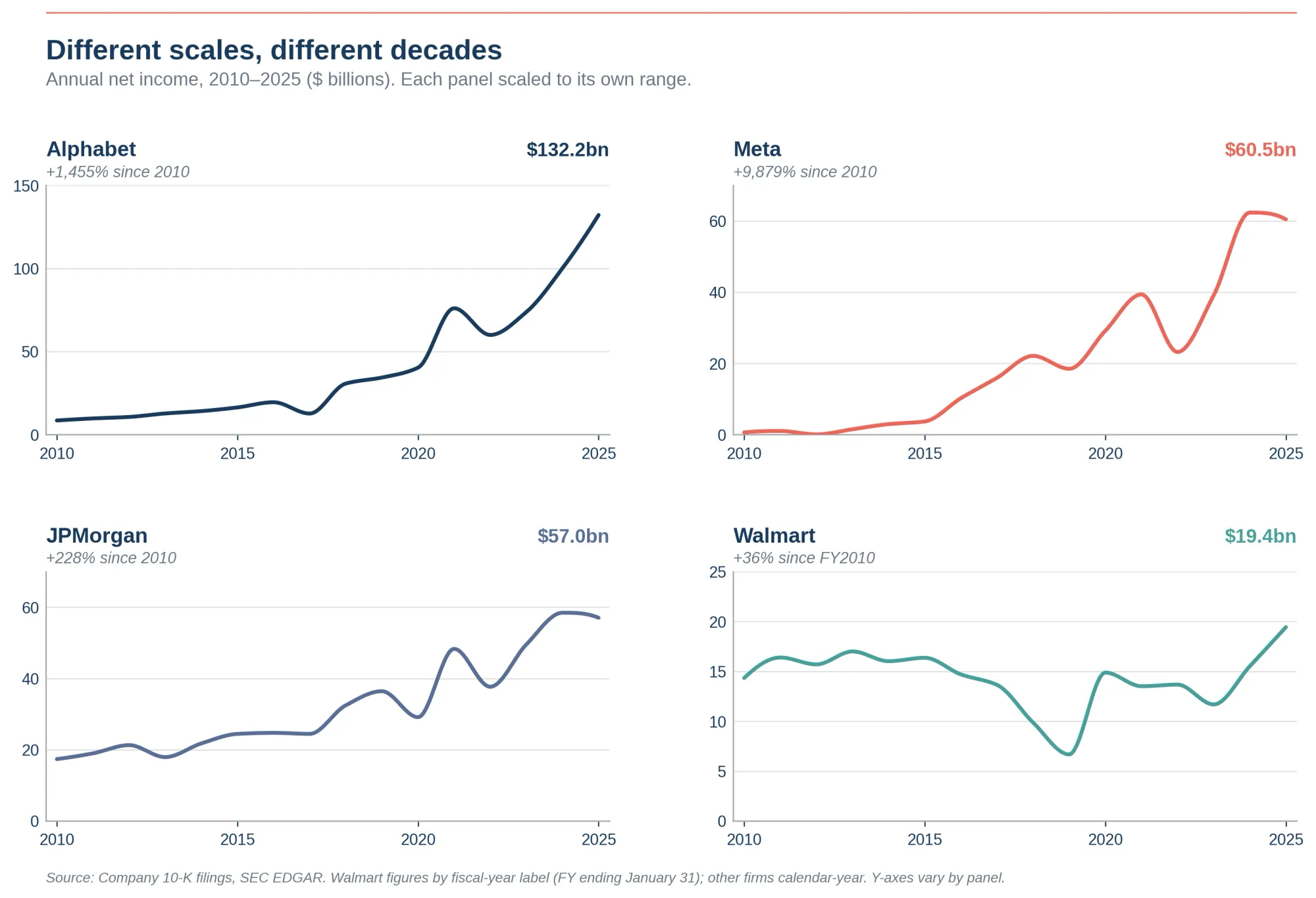

The world's largest retailer earned $19.4 billion in net income in 2025. The most profitable bank in American history earned $57 billion. The tech giant with 3 billion daily users across Facebook, Instagram, WhatsApp, and Messenger earned $60.5 billion. Alphabet, formerly known as Google, earned $132.2 billion.[1] The supposedly fading ad-tech company outearned Walmart, JPMorgan Chase, and Meta combined.

The financial press has spent three years filing Alphabet away as old news. Beaten by OpenAI in consumer AI. Beaten by Microsoft in enterprise distribution. Trading at a discount to Nvidia and Meta on most growth multiples. Sundar Pichai cast as the AI laggard. Nevertheless, by net income, Alphabet is the most profitable enterprise in human history. The consensus has the company exactly backwards.

Understanding why requires understanding what Alphabet actually sells.

What Walmart and JPMorgan tell you about scale

Walmart is the largest physical business on earth by revenue. It moves more than $700 billion of goods annually, employs 2.1 million people, and serves roughly 240 million Americans every week. There is no larger retail operation. There is no plausible path to building one. Walmart's 2025 net income was $19.4 billion. Retail margins run 24 percent gross, 4 percent operating, 2.7 percent net. No amount of scale changes those numbers. The retail business has a ceiling, and Walmart has hit it.

JPMorgan Chase is the apex of American finance. Jamie Dimon spent two decades assembling the most powerful balance sheet in the country: the consumer bank, the corporate and investment bank, asset management, and the trading desk that ate Wall Street after 2008. JPMorgan earned $57 billion in 2025, the most of any bank in American history. That figure represents the upper limit of what a regulated financial institution can extract from the U.S. economy under the current Basel framework.[2] Capital requirements, leverage ratios, and credit cycles will inherently cap future growth.

Meta is the most informative of the three comparisons. The company has built the largest audience in the history of communication: 3 billion daily active users across Facebook, Instagram, WhatsApp, and Messenger. Every adult in the developed world is on at least one of its surfaces. The social graph it has assembled is the most valuable network ever built. By every metric of human attention captured, Meta should be the most profitable company that has ever existed. Meta earned $60.5 billion in 2025, less than half of what Alphabet earned the same year.

Three of the most dominant businesses ever built, each dominating its category, and none of them come close to Alphabet. One specific business model is operating at another level entirely.

Intent is the asset class

Meta sells attention. Alphabet sells intent. The distinction sounds small. The economics are not.

A user scrolling Instagram is in a low-intent state. They are passing time, mildly engaged, open to being entertained. The advertiser bidding to reach that user is paying to interrupt the scroll with a brand impression that may convert at some unspecified future moment, through a path the advertiser cannot trace. The CPM is real but the conversion economics are diffuse. Multiply diffuse conversion economics by 3 billion users and you get Meta's $60 billion in net income, which is an enormous number, and which is also a fraction of what the same advertising dollar produces when it is deployed differently.

A user typing "best dishwasher under $800" into Google search is in the highest-value commercial state any human can be in. They are actively trying to spend money. They have raised their hand. They are two clicks from a purchase. The advertiser bidding on that query is paying for a customer at the point of decision. The CPM and the conversion rate operate on a different curve from anything in the attention business.[3] Google has spent twenty-five years building and perfecting the infrastructure that, at the moment, is the most valuable piece of real estate in the global economy.

This is why 3 billion daily users on Meta's platforms generate less than half the profit that Alphabet generates. The 3 billion users are doing different things on Meta than they are doing on Google, and what they are doing on Google is worth dramatically more per second of engagement. The most lucrative business model ever invented turns out to be owning the moment of commercial intent. Capturing the largest audience in human history is the second prize.

Walmart, the destination after the buying decision has been made, is even further from the value. The Walmart shopper has already decided to buy laundry detergent; Walmart's profit comes from the markup on physical goods sold to a customer who is no longer making a choice. JPMorgan is in a different kind of intent business, capital intent rather than commercial intent, and the regulated nature of finance means the bank cannot capture more than a small share of the value that flows through it. Alphabet's position is structurally unique. The company sits at the moment of commercial choice, the moment is global, the moment is digital, and Alphabet has the only complete index of it.

Why AI grows the moat rather than shrinks it

The consensus argument runs as follows: ChatGPT replaces search, users stop coming to google.com, the ad-supported query funnel collapses, and Alphabet's economics revert toward Meta's or worse. This has been the dominant reading since late 2022. It is wrong. Alphabet's net income grew from $59.9 billion in 2022 to $132.2 billion in 2025, a 121 percent increase during the period when ChatGPT was supposedly cannibalizing Google’s core search business.

The consensus confuses thinking with deciding. People go to ChatGPT to think out loud, to explore ideas, to draft, to learn. The advertiser will pay handsomely to be seen by someone deciding, and pay almost nothing to be seen by someone thinking. The commercial query, the comparison shopping moment, the "near me" search, the high-intent transactional moment all continue to flow through Google, and there is no obvious mechanism by which they would migrate. Google is doing what it has always done at the moment of choice, just better, because Gemini-powered search now answers the query directly inside the same surface where the ad inventory sits.

The Apple-Siri deal is an important proof point. In late 2025, Apple announced it would use Gemini to power the rebuilt Siri.[4] Apple is the only company on earth with the balance sheet, talent, and operating system control to build a credible AI assistant of its own. Instead, Apple chose to pay rent to Alphabet. The reason is that Siri has failed at commercial-intent queries for fifteen years, and Google is the only company that has spent twenty-five years indexing what people want to buy. Apple cannot build that. Apple cannot buy that. Apple has to rent it. The deal makes Alphabet the AI infrastructure layer underneath the most lucrative consumer hardware platform in the world.

The capex cycle reinforces the position. Alphabet has guided to $175-185 billion in capital expenditure for 2026, roughly double its 2025 spend. Cloud backlog reached $240 billion at year-end 2025, more than tripling year over year. Google Cloud is growing at 48 percent.[5] The company is funding a generational AI compute buildout out of cash flow generated by the search ad business, and using the buildout to entrench the search ad business further. No other firm in the global economy has access to a cash machine that funds its own moat at this scale.

The legal pressure does not change the trajectory. When Judge Amit Mehta declined to break up Google in September 2025, Alphabet stock rose 8 percent. Wedbush titled its analyst note "Government Folds Like Cheap Suit." A separate ad-tech case before Judge Leonie Brinkema found Google liable in April 2025, and the remedies phase is ongoing.[6] The timeline matters. Antitrust runs on regulatory time: years to decisions, years more to implementation. The platforms operate on capex time: quarterly guidance, eighteen-month buildouts. By the time any structural remedy lands, the AI compute moat will have deepened by hundreds of billions of dollars. The legal system is litigating yesterday's monopoly while tomorrow's is being built in concrete and silicon.

What this means for the political economy

The political imagination of the United States is wired for an economy in which dominant firms employ millions of people, anchor cities, and serve as institutional ladders by which ordinary Americans move into the middle class. General Motors at its peak employed more than 600,000 people. U.S. Steel employed 340,000. AT&T at the moment of its breakup employed nearly a million.[7] The largest American firm of the postwar era was, by definition, also one of the largest American employers. Size and headcount scaled together.

No longer. Alphabet employs roughly 183,000 people. Meta employs about 76,000. The four largest American technology firms by market capitalization — Alphabet, Microsoft, Nvidia, and Apple — together employ fewer people than General Motors did at its peak. Walmart, the lowest-earning of the four firms compared here, employs 2.1 million Americans, more than ten times Alphabet's payroll. The most profitable enterprise in human history operates with a workforce that would not fill a mid-sized American city.

The political system has not absorbed this. The S&P 500 has become an index where the top ten firms account for 41 percent of total market capitalization, up from 23 percent in 2000 and roughly 18 percent through most of the 1990s.[8] Capital is concentrating into firms that need fewer workers per dollar of output than any prior generation of large companies. The labor share of corporate income has been drifting downward for two decades. The AI cycle will compress it further.[9] Alphabet sits at the leading edge of an arrangement in which unprecedented corporate wealth is generated by extraordinarily small numbers of people, while the institutional channels that historically distributed that wealth (wages, employment, regional economic anchoring, union bargaining, the corporate income tax base) are weakening simultaneously.

The country has not chosen this. There has been no national debate about whether the United States wanted an economy in which the most profitable enterprises ever built require the fewest workers, face the weakest regulatory checks, and answer only to capital markets. The arrangement was constructed company by company, deal by deal, ruling by ruling, while the political conversation focused elsewhere. Walmart and JPMorgan represent the old order: enormous, embedded in millions of lives, bounded by the physical and regulatory constraints that historically connected corporate scale to social presence. Alphabet represents the new order: more profitable than either, embedded in fewer lives, bound by no comparable constraint.

The central political question is whether a democratic society can sustain itself when its most economically powerful institutions operate independently of the very citizens whose attention, data, and intent they have spun into corporate gold. That question has not been asked seriously. The next decade of American economic and political life will be largely about what happens when it is.

Notes

All 2025 net income figures from company 10-K filings, fiscal year 2025. Walmart's fiscal year ends January 31, so figures here reflect FY2026 (the year ending January 31, 2026), the closest comparable annual period; Alphabet, JPMorgan, and Meta are calendar-year. Net income attributable to common shareholders. ↩︎

JPMorgan's $57 billion in 2025 net income was a slight decline from its 2024 record of $58.5 billion, and represents the highest annual earnings ever reported by a U.S. bank. The Basel III framework as currently implemented in the United States caps leverage at levels that constrain return on equity to roughly 17-20 percent for the largest banks; JPMorgan operates near the upper end of that range. ↩︎

Industry CPM data illustrates the gap. Meta's average ad CPM runs roughly $7-12; Google search ad CPM on high-intent commercial queries can exceed $50, with conversion rates several multiples higher because the user has already self-identified as a buyer. ↩︎

Apple announced the Gemini-powered Siri rebuild in late 2025 as part of a broader AI services agreement with Google, reported by multiple outlets including CNBC and the Financial Times in early 2026. Alphabet management cited the Apple deal repeatedly during its Q4 2025 earnings call as evidence of distribution strength. ↩︎

Capex guidance and cloud backlog figures from Alphabet's Q4 2025 earnings release, February 2026. The $240 billion cloud backlog represents future contracted revenue, more than doubling year-over-year. Combined 2026 capex from the four largest U.S. hyperscalers (Alphabet, Microsoft, Amazon, Meta) is projected at $635-665 billion, larger than the GDP of Sweden. ↩︎

Two separate antitrust cases. The search monopoly case (United States v. Google, D.D.C.) concluded the remedies phase in September 2025 with Judge Mehta declining structural divestiture. The ad-tech case (United States v. Google, E.D. Va.) found Google liable in April 2025 on two of three counts; remedies are pending. Both rulings are subject to appeal, with final resolution unlikely before 2027-2028. ↩︎

Historical employment figures: General Motors peaked at approximately 618,000 employees in 1979 (since reduced to roughly 162,000); U.S. Steel employed 340,000 at its 1943 peak; AT&T employed approximately 1 million at the time of the 1984 Bell System divestiture. ↩︎

S&P 500 concentration data from S&P Dow Jones Indices and RBC Wealth Management research, 2026. The top-10 share reached 41 percent in 2025, the highest concentration in the index's history, exceeding the previous peak during the 2000 dot-com bubble. ↩︎

Labor share trends from BLS and the Federal Reserve Bank of San Francisco. The labor share of nonfarm business sector income peaked at roughly 65 percent in 1970 and has trended downward to approximately 58 percent in 2024. Goldman Sachs Research projects AI adoption could accelerate this decline by 1-2 percentage points over the next decade in their base case. ↩︎