Global Growth May Be Doomed

Dark clouds on the growth horizon

A short intelligence memo on Strategic Competition. Read for the core judgment, evidence trail, and decision implication.

Dark clouds on the growth horizon

- Frame

- Briefing

- Topic

- Strategic Competition

- Access

- Free

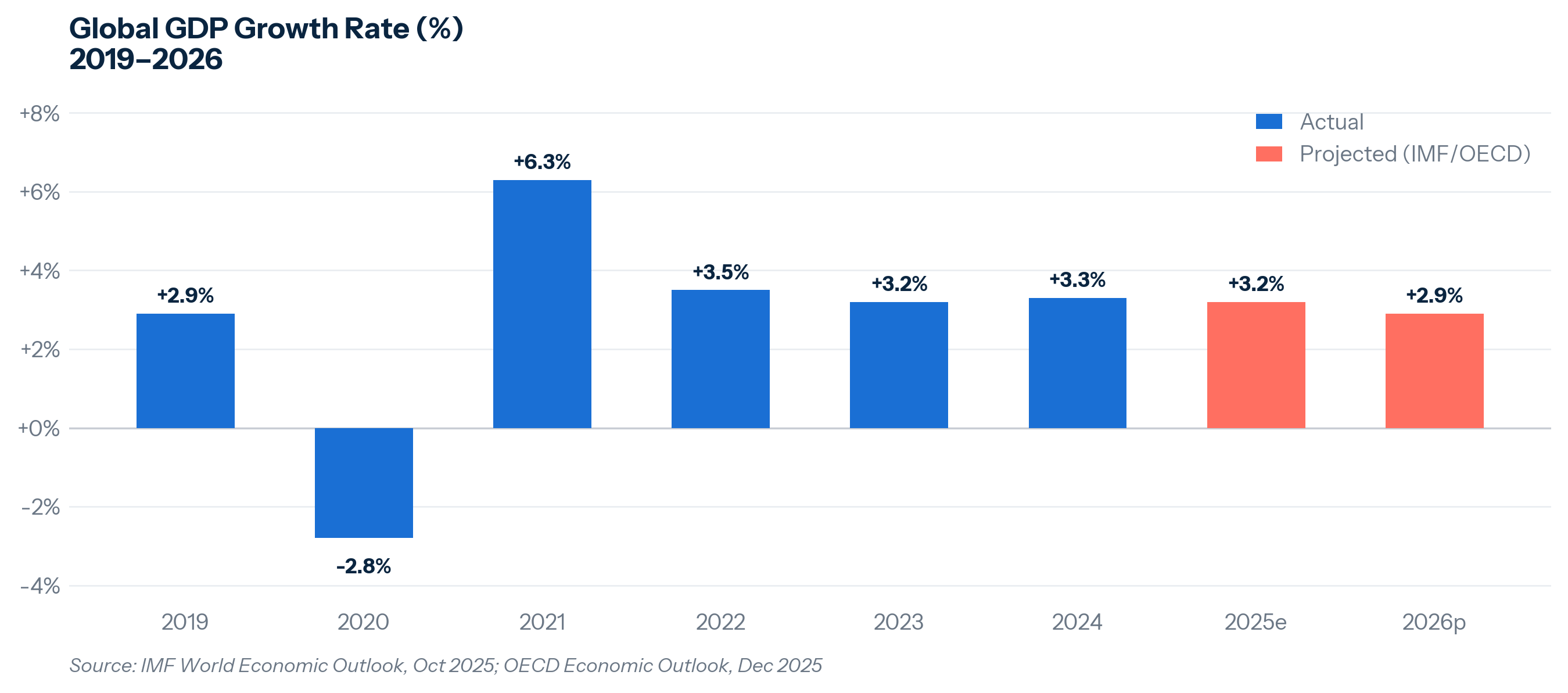

GDP growth is the most fundamental measure of economic health: it tells you whether a nation — or the world — is producing more goods, services, and income than it did the year before. A world growing at 4% is one where living standards double roughly every 18 years. At 2.9%, that doubling takes 25 years. The difference compounds across generations in ways that dwarf any single policy decision or market cycle.[1]

The post-World War II era established the modern growth baseline. From 1950 to 1973, advanced economies averaged 4–5% annually, fueled by reconstruction, industrialization, and the mass adoption of consumer technology.[2] The decades that followed were turbulent — the 1973 oil shock, the Latin American debt crisis, the Asian financial crisis, the dot-com collapse — yet long-run average growth held between 3.5% and 4%.[3] The global economy, it seemed, had a floor.

Then 2008 happened.

The Global Financial Crisis was more than a severe recession. It was a balance-sheet crisis that left advanced economies saddled with debt, suppressed investment, and structurally lower demand for years afterward. Average growth in the 2010s slowed to 3.2% globally.[4] This is when "secular stagnation" entered the mainstream — Lawrence Summers' hypothesis that advanced economies had entered a period of chronically depressed growth driven by demographic aging, slowing productivity, and a structural excess of savings over investment.[5] The political class talked about it endlessly. Little was done.

The Covid pandemic delivered the sharpest single-year contraction since the Great Depression, with global output falling 2.8% in 2020. The subsequent rebound — U.S. growth reached 6.3% in 2021 — was real but misleading: it was driven almost entirely by pent-up demand and an extraordinary surge of fiscal stimulus, not by any durable improvement in the economy's underlying productive capacity. Once conditions normalized, growth returned almost precisely to its post-2008 trend. The IMF projects 2.9% for 2026; the UN forecasts 2.7%.[6]

Not a crisis. Far short of 4%.

| 2025 Estimate | 2026 Projection | Pre-Pandemic Avg | 2000–19 Avg |

| 3.2% | 2.9% | 3.2% | 3.8% |

Not Just Another Slowdown

What makes the current slowdown more troubling than the post-2008 episode is that it appears structurally driven rather than cyclically driven — meaning there is no obvious recovery waiting on the other side. China, which contributed roughly one-third of all global growth between 2000 and 2020,[7] is slowing as its property sector contracts and its working-age population enters structural decline. The demographic arithmetic is unforgiving: China will grow old before it grows rich, and the economic model that powered its ascent has run into walls it cannot spend or export its way through.[8]

The United States, rather than pressing its structural advantages, has complicated its own position. The Trump administration's tariff regime functions as a supply-side tax — raising costs for domestic producers and consumers while inviting retaliation from trading partners. Goldman Sachs estimates current tariff levels are subtracting 0.3–0.5 percentage points from U.S. growth alone.[9] At a moment when the global economy is already operating below its productive potential, that is not a rounding error.

Watch This Space

GDP growth is not an abstraction. It connects directly to corporate earnings, unemployment rates, the sustainability of national debt, and the level of interest rates that governments and households can afford to carry. When growth is strong, fiscal pressures ease, investment flows, and distributional conflicts soften. When growth is weak, the opposite is true: governments face harder choices, competition for investment intensifies, and the politics of scarcity tend to replace the politics of expansion.

If 2.7–2.9% is the new structural ceiling for global growth — not a trough to recover from but a regime to operate within — the implications are significant. Watch three things: whether China's slowdown stabilizes or accelerates into a harder landing; whether U.S. trade policy reverses course before the damage compounds; and whether any major economy produces a credible productivity shock, likely through AI or energy transition, large enough to shift the trajectory.

Absent one of those developments, the era in which growth quietly resolved fiscal, political, and distributional tensions is over.

World Bank, Rule of 70, World Development Indicators (2024). ↩︎

Angus Maddison, The World Economy: Historical Statistics, OECD Development Centre (2003). ↩︎

IMF, World Economic Outlook Historical Data, various editions (1980–2007). ↩︎

IMF, World Economic Outlook, April 2019, Chapter 1. ↩︎

Lawrence H. Summers, 'U.S. Economic Prospects: Secular Stagnation, Hysteresis, and the Zero Lower Bound,' Business Economics 49(2), 2014. ↩︎

IMF, World Economic Outlook, October 2025; UN, World Economic Situation and Prospects 2026; OECD, Economic Outlook, December 2025. ↩︎

IMF, World Economic Outlook, October 2025, Chapter 2. ↩︎

IMF, World Economic Outlook, October 2025, Chapter 2. ↩︎

Goldman Sachs Global Investment Research, US Economic Outlook: Tariff Scenarios and Growth Impact, March 2026. ↩︎