The Split and the Convergence

BlackRock scaled the flow, Blackstone engineered the outcome.

A short intelligence memo on Capital Markets. Read for the core judgment, evidence trail, and decision implication.

BlackRock scaled the flow, Blackstone engineered the outcome.

- Frame

- Briefing

- Topic

- Capital Markets

- Access

- Free

The 1994 rupture between Larry Fink and Stephen Schwarzman produced not two firms but two operating systems for capital. Thirty years later those systems are converging, and the convergence is what matters. The central question is no longer which firm is winning. It is whether the boundary between scale and control can be held by a single institution without breaking either model.

The Split That Created Two Models of Capital

The architecture of contemporary finance can be traced to a disagreement inside Blackstone over compensation, ownership, and long-term direction. Fink left to build what became BlackRock. At the time the conflict looked tactical. In retrospect it was foundational. It separated two fundamentally different approaches to capital.

BlackRock emerged as a system for managing capital at scale, built on risk management, transparency, and institutional trust. Blackstone remained focused on concentrated ownership, active intervention, and high-return opportunities. The split did not simply produce two firms. It divided finance into two operating logics: one in which capital is treated as a flow to be optimized, and another in which capital is treated as an instrument of control.

Why Scale Looks Like Dominance

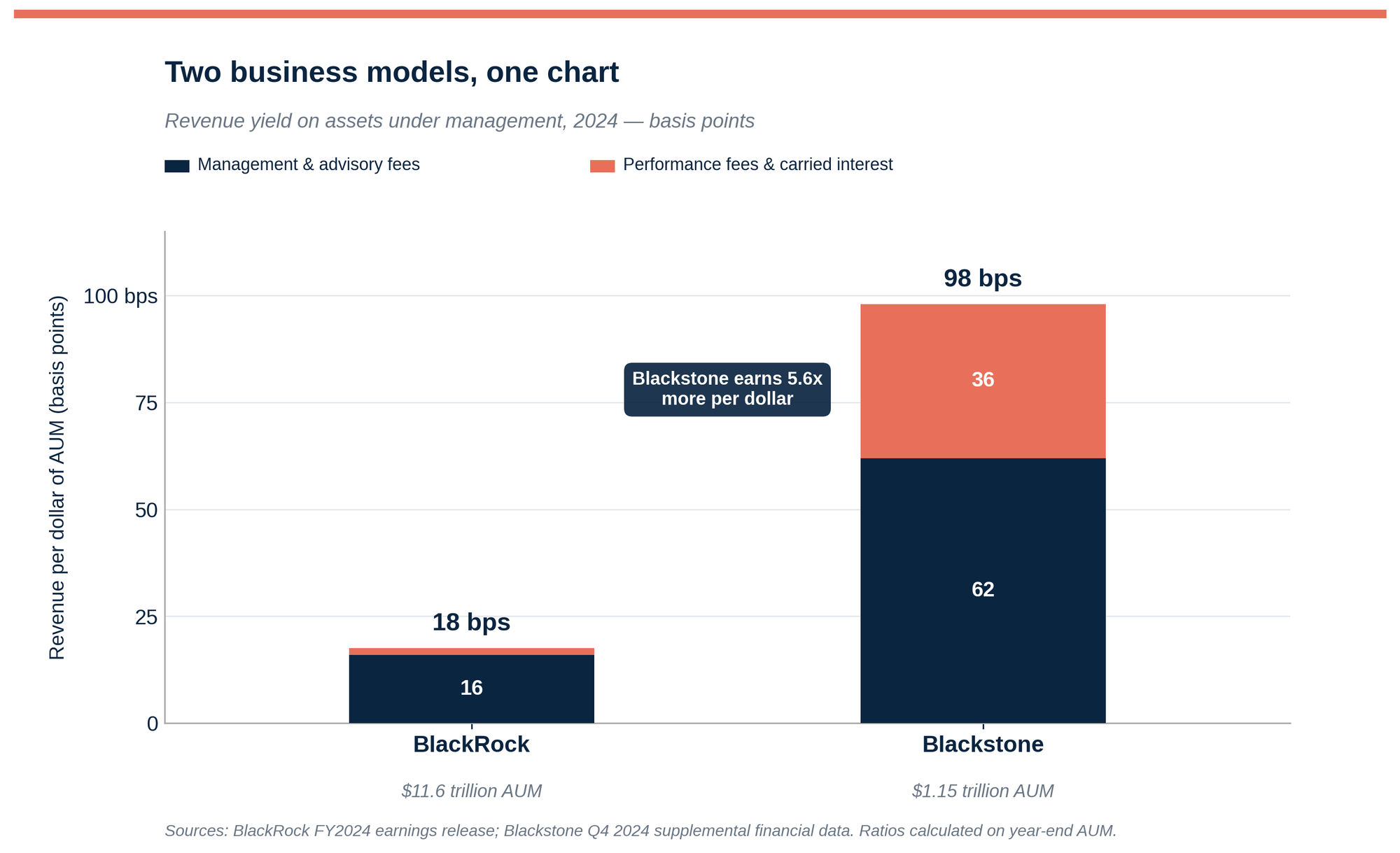

BlackRock now manages roughly $11.6 trillion in assets. Blackstone manages closer to $1.15 trillion.1 That tenfold disparity is commonly read as dominance. The reading is wrong.

Scale in public markets is a function of liquidity and standardization. BlackRock's expansion reflects the industrialization of investing, where exchange-traded funds, index strategies, and institutional mandates transform capital allocation into a high-efficiency system. Its scale does not derive from superior insight into individual assets. It derives from the firm's ability to process and distribute exposure at global volume.

Blackstone operates under different constraints. Private markets require selectivity, governance, and intervention. Capital cannot be deployed indefinitely without eroding returns because opportunities that allow for control are finite. Blackstone's binding constraint is opportunity density, not capital supply.

The divergence in assets under management reflects two different production functions of capital. One is optimized for throughput. The other is optimized for transformation.

What the Arithmetic Shows

Each firm earns a fundamentally different amount of revenue per dollar of assets under management. The gap is structural, and it is large.

BlackRock earns roughly 18 basis points on every dollar it manages. Blackstone earns 98. The gap reflects economic model, not operational efficiency.

The exhibit breaks out each firm's revenue into two components. BlackRock's bar is almost entirely base management and advisory fees. Blackstone's bar is roughly two-thirds management fees and one-third performance revenues, where performance revenues capture carried interest, realizations, and incentive fees tied to specific investments.

This is the heart of the divergence. BlackRock's revenues are measured in basis points and compress over time as public markets become more efficient. Investors pay for access, and the price of access declines. Blackstone captures a share of the profits generated when portfolio companies are restructured, operations are improved, and exits are timed. The firm earns more per dollar because it alters the dollar's destination.

In public markets, value increasingly lies in efficient allocation, which becomes commoditized. In private markets, value remains tied to the ability to alter outcomes. BlackRock monetizes distribution and trust. Blackstone monetizes scarcity and performance.

Why Profit per Dollar Tells a Different Story

Measured in absolute terms, both firms are highly profitable. Measured on a per-dollar basis, the hierarchy inverts.

BlackRock's margins are strong but constrained by fee compression. Its profitability depends on scale, efficiency, and continuous inflows. Blackstone's profitability is episodic but structurally higher on a per-dollar basis, driven by the firm's ability to reshape assets, apply leverage, and exploit inefficiencies.

This reveals the central dynamic of modern finance. The highest returns accrue to those who can intervene in capital's deployment, not merely to those who allocate it most efficiently. BlackRock optimizes the system. Blackstone extracts value from within it.

The Liquidity-Control Trade

The relationship between the two firms can be understood through the lens of liquidity and control. Public markets provide liquidity but limit influence. Private markets reduce liquidity but increase the ability to shape outcomes.

BlackRock operates at the high-liquidity, low-control end of this spectrum, providing efficient exposure to markets as they exist. Blackstone operates at the opposite end, where illiquidity enables active ownership and strategic intervention. These positions reflect structural constraints more than pure strategic choice.

The Convergence Has Names

The distinction between public and private markets is eroding under pressure from investor demand. Capital increasingly seeks both liquidity and yield, while markets traditionally offer one at the expense of the other. The convergence is visible in specific vehicles and specific acquisitions.

BlackRock has moved decisively into private markets. The $12.5 billion acquisition of Global Infrastructure Partners in 2024 added roughly $170 billion in infrastructure AUM at materially higher fee rates than the firm's core index business.2 The July 2025 acquisition of HPS Investment Partners added approximately $157 billion in private credit.3 The economic logic is fee-rate arbitrage: BlackRock is buying its way out of compression.

Blackstone has moved in the opposite direction. Perpetual-capital vehicles now constitute roughly 40 percent of its fee-earning AUM.4 The Blackstone Real Estate Income Trust (BREIT) and the Blackstone Private Credit Fund (BCRED) extend private-market exposure to wealth channels through semi-liquid structures that accept monthly subscriptions and permit limited periodic redemptions. These vehicles convert what was once an institutional product with ten-year lockups into something approaching a retail yield product. Both moves compress the same boundary from opposite sides.

BlackRock is extending reach into higher-margin private assets. Blackstone is extending access to broader investor pools. The convergence is structural, not cyclical.

Leadership Reflects the Underlying System

The leadership of the two firms reflects their underlying architectures. Fink has positioned BlackRock as a system-level institution embedded in global markets, emphasizing stewardship, risk management, and alignment with long-term capital. His influence extends into corporate governance and policy discourse.

Schwarzman has built Blackstone as a performance-driven investment platform defined by conviction, execution, and incentive alignment through carried interest. Under his leadership, the firm has institutionalized a model that rewards decisive intervention and calculated risk-taking.

These approaches express the underlying systems each firm operates within. BlackRock requires trust and stability. Blackstone requires judgment and control.

Where Convergence Meets Its Limits

The convergence thesis is correct but it is not costless. Three frictions will determine whether integration holds.

The first is regulatory. Perpetual-capital vehicles marketed to retail and mass-affluent investors attract scrutiny the institutional private funds never faced. BREIT's 2022 redemption gating episode made the liquidity mismatch visible,5 and regulators in both the United States and Europe have signaled tighter disclosure and leverage requirements for semi-liquid private vehicles.

The second is fee-rate decay. As private credit and private infrastructure become more competitive, the fee premium that justifies the acquisitions compresses. BlackRock is paying public-market multiples for private-market fee rates that may not hold at scale.

The third is organizational. Scale cultures and control cultures do not blend easily. Index businesses reward standardization, low cost, and system reliability. Private equity and credit businesses reward selectivity, judgment, and patience with illiquidity. Running both inside a single firm requires compensation structures, governance models, and risk frameworks that pull in different directions.

What to Watch

Three indicators will confirm or weaken the integration thesis over the next three years. Whether BlackRock's private-markets fee rates hold above 40 basis points after GIP and HPS integration. Whether Blackstone's perpetual-capital AUM crosses 50 percent of fee-earning AUM without a second gating event. And whether either firm produces a successor generation capable of operating at the scale-control boundary rather than on one side of it.

Bottom Line

The 1994 split produced two curves of capital. For three decades they operated in parallel. They are now intersecting, and the firms that integrate them without breaking either model will set the terms of capital deployment for the next decade. BlackRock is no longer only an asset manager. Blackstone is no longer only a private equity firm. Each is attempting to become something the other has never been. The firm that completes the crossing first will dominate finance by being the only institution that both governs the flow and engineers the outcome.

The split explained the past. The convergence will explain what comes next.

Notes

- BlackRock AUM as of December 31, 2024. BlackRock, "BlackRock Reports Full Year 2024 Diluted EPS of $42.01," January 15, 2025. Blackstone AUM as of December 31, 2024. Blackstone, Fourth Quarter 2024 Supplemental Financial Data, January 2025. ↩

- BlackRock, "BlackRock Completes Acquisition of Global Infrastructure Partners," press release, October 1, 2024. Combined infrastructure platform AUM of approximately $170 billion at close. ↩

- BlackRock, "BlackRock Completes Acquisition of HPS Investment Partners," press release, July 1, 2025. HPS AUM of approximately $157 billion as of March 31, 2025. ↩

- Blackstone, Fourth Quarter 2024 Supplemental Financial Data. Perpetual-capital AUM as a share of fee-earning AUM. ↩

- Blackstone Real Estate Income Trust began limiting monthly redemptions in November 2022 after requests exceeded the 2 percent monthly and 5 percent quarterly thresholds. BREIT fulfilled its full redemption backlog for the first time in February 2024. Blackstone shareholder letters, December 2022 through March 2024. ↩