President Trump made his expectations plain at the swearing-in. “I want Kevin to be totally independent,” he said in the East Room on May 22, then turned to his nominee and added, “Don’t look at me, don’t look at anybody, just do your own thing and do a great job.”1 The room understood the subtext. Trump had spent more than a year demanding lower rates, pursued a criminal probe of Jerome Powell, and engineered the most contested Fed succession in modern history, with the Senate confirming Warsh in a 54 to 45 vote, the closest margin on record.2 The new chairman was supposed to deliver the cuts.

Warsh did the opposite, and the move is more deliberate than a simple act of defiance. In his first month he held rates steady, presided over a forecast that now points toward a hike, and announced the broadest reexamination of Federal Reserve practice in a generation. Those reforms are the tell. By refusing Trump’s cuts now and rebuilding how the Fed defines and measures inflation, Warsh is assembling the credibility and the analytical case to lower rates later, on a timetable and a rationale he alone controls. The hawkish opening is the first move in an easing strategy, executed on his own terms.

His return alone is an institutional rarity. Warsh served as a Fed governor from 2006 to 2011, appointed at 35 as the youngest in the Board’s history, seated beside Ben Bernanke through the 2008 crisis before he resigned amid his discomfort with the scale of quantitative easing.3 Nearly eight decades had passed since a former governor came back to chair the Board. He arrives now at 56, the wealthiest chair ever to hold the office, under a four-year term that runs to May 2030.4

The setting gives his arrival its charge. Inflation has run above the Fed’s 2 percent target for more than five years, a failure that began with the “transitory” misjudgment of 2021 and 2022 and deepened this spring when the war in Iran drove energy prices higher. Consumer prices rose at a 4.2 percent annual rate in May, the steepest in more than three years, though core inflation held lower at 2.9 percent.5 Against that record, Warsh’s call for “regime change,” first made in a television interview in 2025, found a receptive audience among critics who believe the institution lost its discipline.6 It also lands inside a constitutional contest. The administration pursued the Powell probe, continues an effort to remove Governor Lisa Cook now before the Supreme Court, and presses openly for easier policy. Warsh therefore inherited a central bank whose independence was already the subject of litigation, congressional hearings, and daily pressure from the man who appointed him.7

The hawkish hold

The June 17 decision read two ways at once. The Federal Open Market Committee voted 12 to 0 to hold the federal funds rate in a range of 3.50 to 3.75 percent, where it has stood since December 2025 after three quarter-point cuts last autumn.8 The unanimity was its own statement. Powell’s final meeting in April had split 8 to 4, the most divided the committee had been since 1992.9 Warsh handed the new era a clean line.

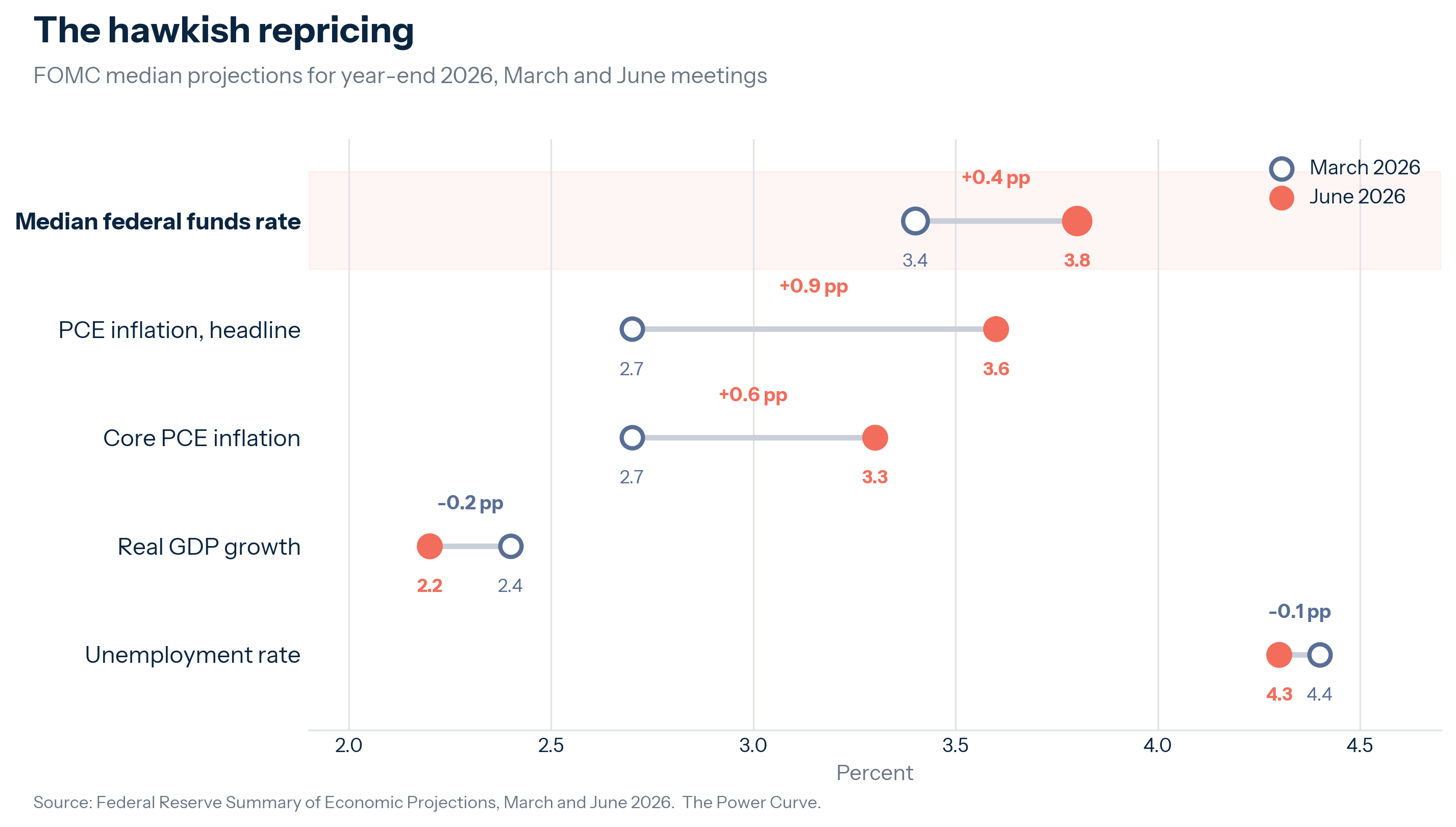

The projections underneath carried the harder message. The median policymaker now expects rates to finish 2026 higher than today, a turn from March, when the median still implied a cut. Nine of eighteen participants project at least one hike this year, six of them two, and seventeen of eighteen judge the risks to inflation as tilted to the upside.10

Exhibit 1

Two quieter moves mattered more than the dots. Warsh gutted the post-meeting statement, describing it as “a bit shorter, a bit simpler” and stripping out the forward guidance that had long signaled an easing bias.11 He also withheld his own projection from the grid, leaving the committee’s most influential voice formally silent on the rate path and calling himself the nineteenth participant who chose not to submit.12 The labor market gave him the room to lean hawkish. Payrolls grew by 172,000 in May, and unemployment held at 4.3 percent, which undercut any case that the economy needed support.13

Markets read the message and repriced within the hour. The two-year Treasury yield, the maturity most sensitive to policy expectations, rose roughly 16 basis points on the day, and the S&P 500 slipped about 0.6 percent. Warsh declined to discuss the selloff, saying he valued the “unfiltered” reaction.14

“I’ve said for years inflation is a choice. You bet it is.”15

The velvet glove

The rate decision was the smaller event. Warsh used his debut to announce five task forces, each pairing internal staff with outside experts and charged with reporting by year-end, that together reexamine nearly every working component of monetary policy: the Fed’s communications, the size and composition of its balance sheet, the data it uses to read the economy, the effect of productivity and artificial intelligence on growth and prices, and the framework for understanding inflation and how it is measured.16 No sitting governor or regional president sits on the panels, a design that lets Warsh import fresh thinking while building consensus from beyond the committee he cannot simply direct.17

The balance-sheet review is the sleeper. Warsh has long objected to the Fed’s bond holdings, now near 6.7 trillion dollars, and to the ample-reserves regime under which the central bank pays banks interest to hold roughly 3 trillion dollars in reserves.18 Following his instincts to their conclusion would mean shrinking the portfolio toward short-term Treasuries alone and restoring a market price for overnight money, the most consequential change to how the Fed operates since the 2008 crisis. One strategist captured the wider ambition as “regime change, but in a velvet glove.”19 No chair in recent memory has opened with a project this broad.

The tests ahead

Credibility is the first test, and it runs through measurement. Warsh argues that supply shocks such as the oil spike should be looked through, and that trimmed-mean inflation, which strips out the most volatile price categories, offers a truer read than the headline figure.20 Paired with his thesis that productivity gains from artificial intelligence are disinflationary, that doctrine gives him a defensible route to ease once energy prices fade.21 The hazard is that markets come to see the framework review as cover for politically convenient cuts. For now he has closed off that reading by holding the 2 percent target and refusing to revisit it “until we have reestablished our commitment and ability to deliver” on it.22

He is also recasting what independence means in practice. Warsh told the Senate he would “absolutely not” be the president’s puppet, and his hawkish opening defied the expectation that he would supply Trump’s cuts. His chosen posture is to keep his head down, captured in the formulation that “Fed independence is up to the Fed,” and in his refusal during confirmation to say plainly whether Trump lost the 2020 election.23 The open Atlanta Fed presidency, the one immediate vacancy on the rate-setting committee, will be the clearest near-term signal of whether he staffs for independence or for alignment.24

The reforms carry a cost he has accepted on purpose. By dropping forward guidance, withholding his dot, and signaling possible changes to the transcripts and the press conference, Warsh is removing the signposts markets have leaned on since 2008, on his conviction that markets function best when they respond directly to incoming data. The size of the two-year’s one-day move is the early price of that bet, and a market relearning how to read a quieter Fed is a market prone to sharper swings.

Whether any of it sticks depends on colleagues he cannot command. Governors serve fourteen-year terms and regional presidents speak their own minds, so the task forces are built to win the committee over, because he cannot impose his will on it, and the velvet glove works only if the committee agrees to wear it.25 The interpretation splits along familiar lines. Free-market reformers read the opening as vindication, a Trump pick who reasserted hawkish discipline and finally opened the balance-sheet question. Veteran Fed watchers counsel patience and warn that the institution’s existing divisions pose a serious obstacle, advising observers to weigh his actions above his words.26 One meeting cannot settle it. Warsh has shown what he wants; the institution has not yet shown whether it will let him have it.

For investors and policymakers, the next two quarters carry more signal than the rate level itself. The September meeting will test his hawkish resolve, since the market-implied path and the committee’s dots have converged toward a possible hike. The task-force reports due by year-end, on the balance sheet and the inflation framework above all, will reveal whether regime change is substance or branding. The Atlanta appointment will show how he defines independence when it costs him something. The path of oil matters most, because the moment energy pressure eases is the moment his look-through doctrine meets the cuts the White House still wants.

A forecast, stated plainly and held to rough odds. The base case, near 55 percent, is a hold for the rest of 2026: the energy shock fades over the summer, inflation drifts back toward 3 percent, and the threatened hike never arrives. A hike runs about 30 percent, the live risk if oil stays high or price pressure broadens from energy into services. A 2026 cut sits near 15 percent, plausible only if crude retreats sharply and the labor market cracks. The more consequential call is for 2027: once the inflation and data task forces report this winter and supply pressure clears, Warsh will have the framework and the standing to begin cutting on his own terms, and a first reduction in the first half of 2027 is the likeliest path. The cuts Trump demanded will probably arrive. They will arrive late, and they will carry the Fed’s name.

Warsh inherited a central bank under political siege and spent his first month reasserting its inflation mandate while quietly rewiring how it works. The opening was hawkish, disciplined, and more ambitious than the rate decision implied. Whether it holds rests on data he does not control and a committee he must persuade.

Figures and quotations reflect information available as of June 24, 2026.