Three months after NVIDIA and Microsoft committed to invest up to $10 billion and up to $5 billion respectively, Anthropic just closed a $30 billion funding round at a $380 billion valuation. Thirty investors participated, led by GIC, Coatue, D.E. Shaw Ventures, Dragoneer, Founders Fund, ICONIQ, and MGX. The full list reads like a who's who of institutional capital: sovereign wealth funds (GIC, QIA, Temasek), growth equity heavyweights (Sequoia, Lightspeed, Insight Partners), asset managers (BlackRock, Fidelity, Morgan Stanley), and quantitative shops like Jane Street.

This happened against a backdrop of staggering capital deployments to commercialize AI at scale. Amazon committed $200 billion this year. Meta allocated $135 billion. Microsoft exceeded $100 billion. Alphabet directed $185 billion. We're watching over $600 billion flow into AI infrastructure in a single year.

The question isn't whether this is a lot of money. It obviously is. The question is what it means—and whether this constitutes rational capital allocation or the kind of collective FOMO that precedes painful corrections.

The Economics of AI

Building frontier AI models has become one of the most capital-intensive activities in the modern economy. Training models cost tens of billions. The infrastructure requirements—specialized chips, massive data centers, energy systems capable of powering small cities—create barriers to entry that exceed almost anything else in technology.

This isn't software in the traditional sense, where marginal costs approach zero and small teams can compete with powerful incumbents. This is top-to-bottom infrastructure–like building railroads or interstate highways. The scale is more similar to launching satellites than deploying code. The economics look more like aerospace or energy than consumer internet.

But unlike previous technology cycles, where costs declined as markets matured, AI exhibits the opposite dynamic. Each generation of models requires more compute, more data, more engineering talent. The companies that can sustain multi-billion dollar quarterly burn rates gain compounding advantages in capability, which translates directly into commercial value.

The competitive math is brutal. If you're not spending at scale, you fall behind. Once you fall behind in capability, customers leave. Once customers leave, you can't generate the revenue to fund the next training run. The gap widens. This dynamic explains why we're seeing capital concentrate so dramatically—and why half measures don't work.

The firms participating in this round understand this. When Jane Street and D.E. Shaw Ventures–quantitative powerhouses with disciplined capital allocation frameworks–write checks at these valuations, they've run the numbers on growth rates and unit economics. Their participation signals something about the underlying revenue trajectory that isn't visible in public reporting.

Who's Investing and Why It Matters

The composition of Anthropic's investor syndicate tells you everything you need to know about how serious institutions view this technology.

Sovereign wealth funds manage multi-decade time horizons. They don't chase trends. They position for structural shifts in how economies function. When GIC, the Qatar Investment Authority, and Temasek participate alongside quantitative investors and institutional asset managers, they're not making a bet on a product category. They're positioning for the reorganization of knowledge work itself.

Singapore, Qatar, and the UAE are treating AI capability the way they've historically treated energy infrastructure and financial positioning—as strategic assets essential to long-term economic competitiveness. These countries have built their modern wealth by identifying critical infrastructure early and securing access. They're applying the same framework to AI.

Consider what that means. Nations that built sovereign wealth funds specifically to prepare for post-oil economies are now deploying that capital into AI infrastructure. That's not speculation. That's strategic planning by governments that think in generation-long time horizons.

The presence of firms like BlackRock, Fidelity, and Morgan Stanley Investment Management reinforces this interpretation. These institutions manage trillions in assets and operate under fiduciary standards that limit speculative positioning. They allocate to AI infrastructure because they view it as foundational to how value gets created in the next economic era.

If this were irrational capital deployment, we'd see different investor profiles—more venture funds chasing growth narratives, fewer institutions with disciplined frameworks, less sovereign participation. Instead, we're seeing exactly the composition you'd expect for critical infrastructure financing.

The Big Question is Sustainable Revenue

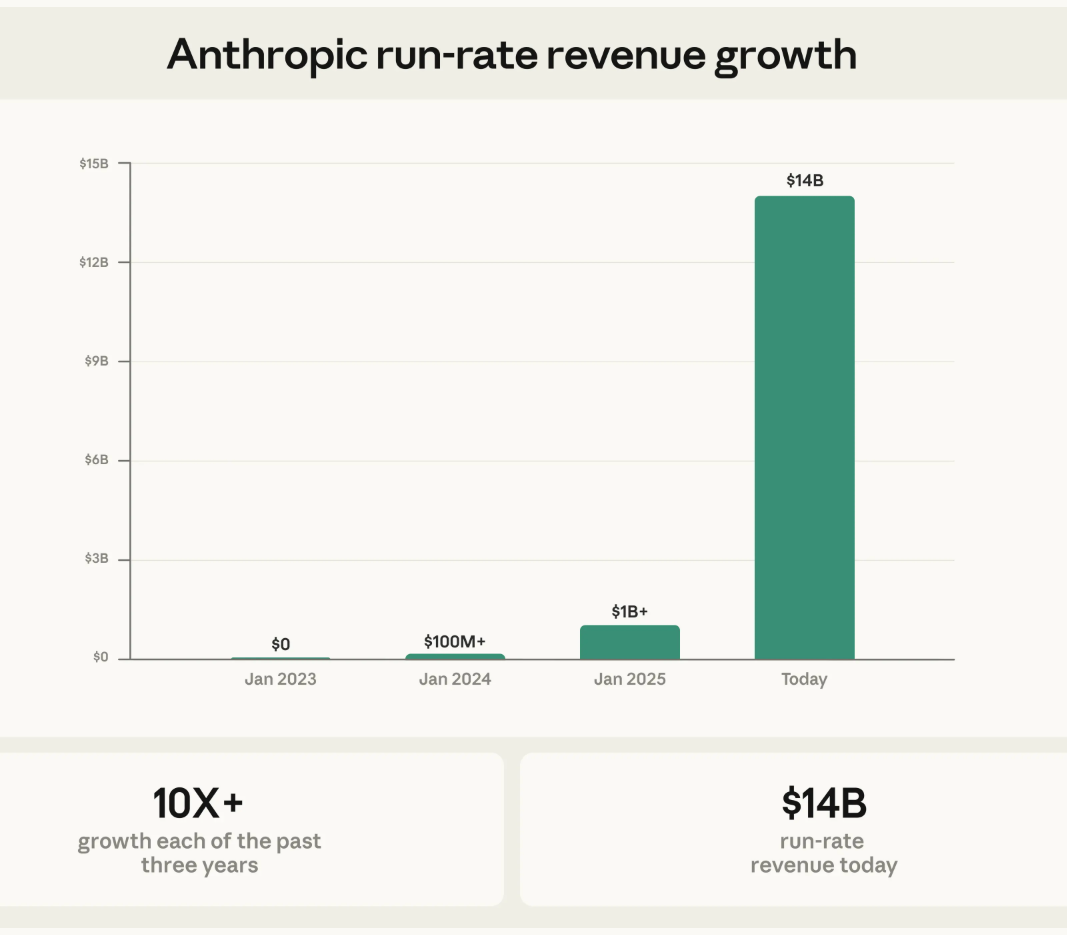

The critical variable is whether Anthropic's valuation reflects demonstrated commercial traction or projected growth expectations. The evidence increasingly points to the former.

Enterprise adoption of Claude has accelerated across professional services, financial analysis, software development, and strategic research. The value proposition is straightforward: Claude performs cognitive tasks previously requiring human expertise at a fraction of the cost with near-instantaneous turnaround. For organizations processing documents, conducting research, or requiring consistent analytical output, the return on investment is measurable and immediate.

Anthropic generates revenue through API consumption, enterprise licensing, and platform subscriptions. The investor composition suggests the underlying numbers justify the price. When quantitative firms like Jane Street participate at this valuation, they've modeled the revenue trajectory and believe the economics work.

The distinction is whether we're looking at steady growth or exponential adoption as capabilities continue improving. Current evidence suggests the latter. As AI systems improve and deployment costs fall, the addressable market expands. Tasks that required $200-per-hour consultants can now be performed for dollars. That's not incremental improvement—that's a phase change in how intellectual work gets priced.

What Such Massive Spending Tells Us

The $600+ billion in aggregate AI spending by Amazon, Meta, Microsoft, and Alphabet reveals something important about competitive markets.

These companies aren't just building AI capabilities. They're building, or attempting to build, durable moats. Amazon's $200 billion includes cloud infrastructure that locks in enterprise customers. Microsoft's $100+ billion protects its productivity and enterprise franchises from displacement. Google's $185 billion represents existential defense against search disruption. Meta's $135 billion reflects a bet that AI compensates for weakening social network economics.

Each company faces a different strategic problem, but they all arrive at the same solution: spend whatever it takes to secure a dominate position in the AI stack. The capital intensity creates natural consolidation. There won't be dozens of companies building frontier models. There will be a handful. And everyone else will build on top of that capital-intensive infrastructure.

Unprecedented Strategic Risk

The concentration of AI capital among a handful of companies creates clear risks for markets and geopolitics.

From a market perspective, we're watching the emergence of a new infrastructure layer. Just as cloud computing created AWS, Azure, and Google Cloud as foundational platforms, AI is creating a similar structure at a higher level of abstraction. The companies that control frontier AI capabilities will function as infrastructure providers for millions of downstream applications.

From a geopolitical perspective, AI capability is becoming inseparable from national economic competitiveness. When JPMorgan Chase participates through its Security and Resiliency Initiative, that signals direct involvement in a complex web of financial system dependencies. When sovereign funds commit billions, that signals nations positioning for an economy where AI capabilities determine competitive advantage across industries.

The real risk isn't that AI doesn't matter. The technology's impact on productivity is already measurable. The risks are context- and interest-specific.

Regulatory constraints could limit deployment faster than companies expect, particularly in Europe where AI governance frameworks are developing rapidly. Technical plateaus could slow capability improvements, changing the economics of continued investment. Safety incidents could trigger political backlash that reshapes the operating environment. Or the brutal attrition of the market could prevent any single company from capturing value proportional to capital deployed—the classic infrastructure trap where importance doesn't equal profitability.

But the most sophisticated capital allocators in the world are convinced these risks are manageable relative to the opportunity. They're betting that whoever builds the most capable AI systems will control critical infrastructure for how intellectual work gets done in the 21st century.

What's Really Being Priced

Anthropic's raise reflects a specific thesis: that AI represents a fundamental shift in how knowledge work happens, and that the companies building the most capable systems will generate, and capture, extraordinary value.

Some evidence supports this interpretation. The investor composition, the scale of capital being deployed across the sector, the measurable productivity improvements in early enterprise deployments, the strategic positioning by both companies and nation-states—all of it points toward AI as fundamental infrastructure, not as another software category.

If AI systems continue improving while costs start to decline, these investments are pricing the transformation of legal research, financial analysis, software development, strategic planning, scientific research, and virtually every other form of knowledge work. The economic implications extend beyond any single company or sector.

Far from hype, that's a rational assessment of what happens when you can automate energy- and talent-intensive tasks at scale. The companies that build those capabilities will have built, and will very likely own, the knowledge layer for the next economy.

The smart money is positioning accordingly.