The Federal Open Market Committee left its policy rate at 3.5 to 3.75% on June 17, a unanimous decision that markets had fully priced. The decision is not the story. The story is that the Committee deleted the language signaling future cuts and, in its own projections, leaned toward members placing the appropriate year-end rate above today's range rather than below it. The driver is an inflation that is not merely sticky but rising, fed by tariffs, a Middle East energy shock, and a demand surge from the artificial-intelligence buildout that the Fed has no interest in extinguishing. The base case is an extended hold; the risk around it now tilts toward firming, not easing.

The Supply Shock Meets the Demand Boom

The Fed is caught between two forces it cannot reconcile with a single instrument. Inflation is climbing, which forecloses a cut. But the largest new source of that inflation is the same AI investment supercycle that is underwriting the expansion, keeping the labor market balanced and productivity strong. Cutting would pour fuel on a demand boom the Committee is otherwise happy to have. Tightening hard would risk the one part of the economy doing the heavy lifting. So the Committee did the only thing the arithmetic allowed: it held, and it removed its own bias toward easing, buying optionality in both directions while betting that the next surprise is more likely to be hot than cold. This is a central bank that has stopped waiting to cut without yet committing to hike.

What Actually Changed

The hold was mechanical. The signal sat in the words the Committee chose not to repeat. Members agreed to strip the postmeeting statement of language that had implied an easing bias, the standing lean toward lower rates that had shaped expectations for months.1 Removing it is not neutral housekeeping. It tells markets to stop assuming the next move is down. A majority also favored shortening the statement outright, and the Chairman announced five independent task forces to review the broad conduct of monetary policy, a signal that the framework itself is in motion rather than settled.1 The plumbing held steady beneath all of this: money markets were stable, reserves remained ample, and the Committee reaffirmed its ample-reserves regime without amendment.

Prices Aren't Behaving

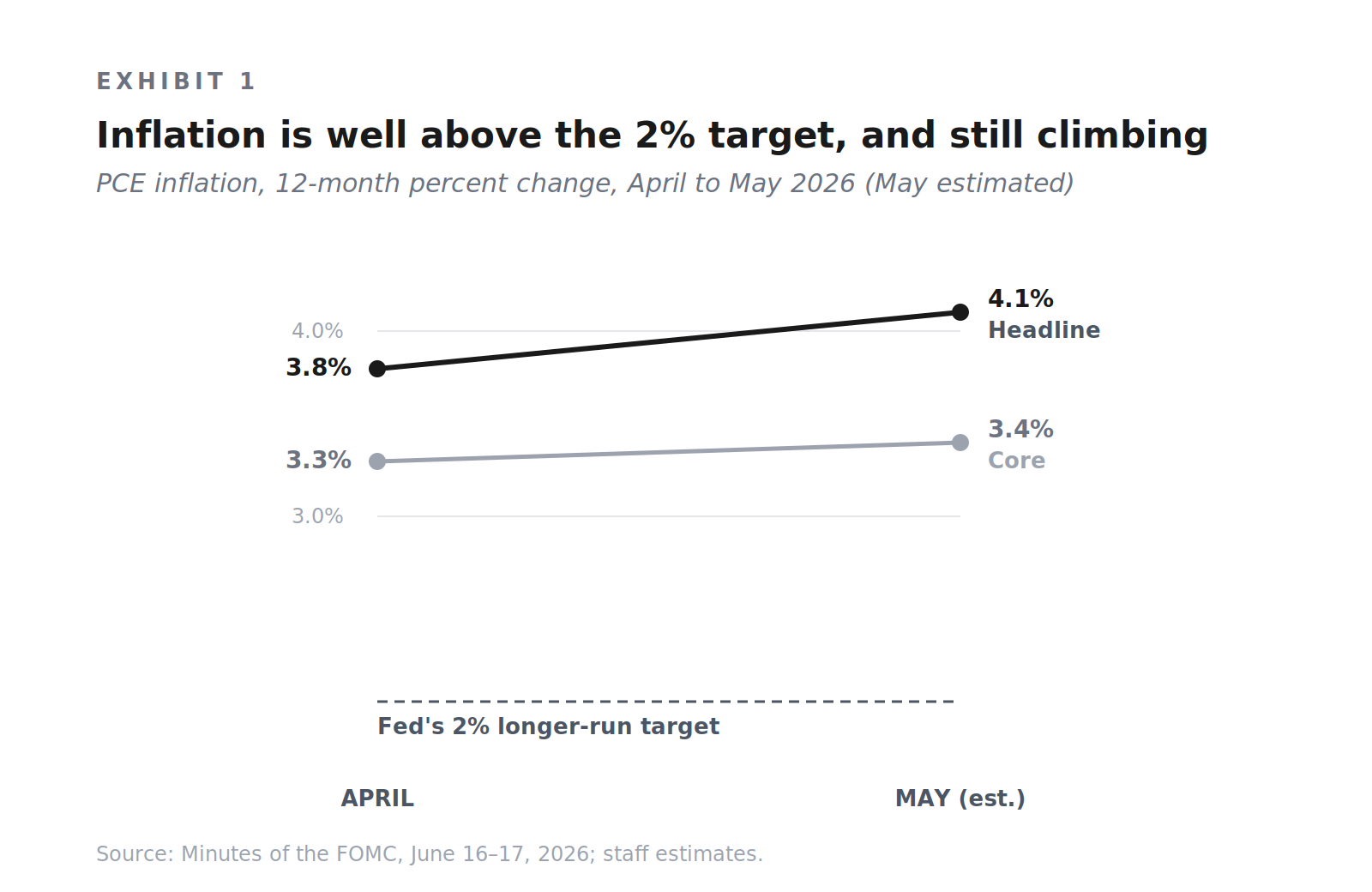

The problem is not that inflation is stuck. It is that inflation is accelerating. Headline PCE inflation, the Fed's preferred measure of consumer prices, ran at 3.8 percent in the year to April, with core inflation, which strips out volatile food and energy to expose the trend, at 3.3 percent. Staff estimated both moved higher still in May, to roughly 4.1 percent headline and 3.4 percent core.1

More troubling than the level is the breadth. Several participants noted that price pressure had spread well beyond the usual suspects into transportation, airfares, petrochemicals, and agricultural inputs, the signature of a broad-based rather than sectoral problem.1 The Committee traced the pressure to three compounding sources: the lagged pass-through of earlier tariffs, an energy shock from conflict in the Middle East and the closure of the Strait of Hormuz, and demand strong enough to lift prices for technology hardware and electricity.

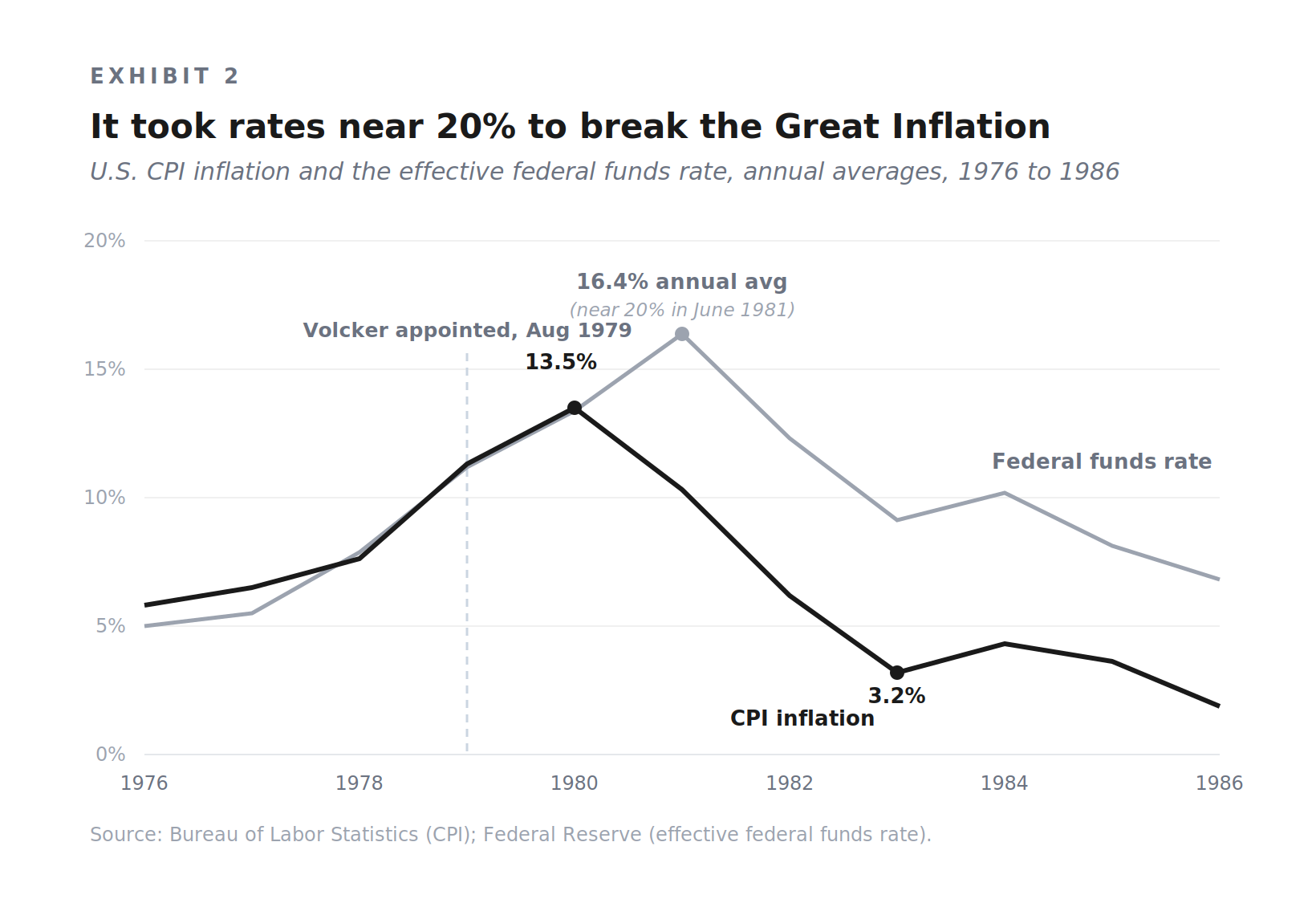

History is why this worries them. After five consecutive years of inflation above target, the Committee's central fear is no longer any single print but the possibility that persistence resets how households and firms expect prices to behave. The reference case is the Great Inflation of the 1970s and the price the Fed paid to end it: to break consumer inflation that had peaked above 14 percent in 1980, Paul Volcker drove the federal funds rate to nearly 20 percent and tolerated unemployment of 10.8 percent by late 1982, the highest since the Depression.2 That is the asymmetry the Committee is pricing. Letting expectations drift is cheap until it is ruinous. Longer-term inflation expectations remain anchored near 2 percent for now, which is precisely the asset the Committee will not gamble by easing early.1

Why It Can't Just Cut

The conventional reading of rising inflation is that the Fed is behind and should tighten. The more useful frame is that the Fed is boxed in by the source of the inflation. Real GDP is expanding at roughly its potential rate, and the engine is business investment concentrated in AI, spending that participants described as showing no signs of slowing, with firms announcing capital plans that keep exceeding expectations.1 That investment is the good news and the complication at once. It sustains growth and employment, and it simultaneously generates the very demand lifting prices for compute and power. The relief that AI eventually promises, higher productivity expanding the economy's supply capacity and pressing costs down, is real but lagged; participants expect it to trail the demand boost by a meaningful interval.1 A rate cut today would accelerate the demand and do nothing for the supply. Holding is the only setting that does not deepen the problem it is meant to solve.

The Labor Market Bought the Freedom

The Committee could lean this hard on prices because the other half of its mandate gave it room. Unemployment held at 4.3 percent in May, little changed over the year and close to estimates of its sustainable level, with payroll gains solid and roughly matched to labor-force growth.1 Most participants judged that the labor market was not currently a source of inflationary pressure and that wage growth remained consistent with inflation eventually returning to target.1 Earlier-in-the-year anxiety about a hiring slowdown had faded. A balanced labor market is what converts a difficult inflation problem into a manageable one: it lets the Committee treat price stability as the binding constraint. The distributional strain beneath the aggregate is worth naming, because it is where the next political pressure will originate. Higher-income households, cushioned by a stock market that rose nearly 6 percent over the period and by tax refunds sent earlier in the year, carried spending; lower-income households leaned increasingly on credit and absorbed the brunt of elevated gasoline and grocery prices.1

The clearest evidence that this was a hawkish hold lies in the Committee's own projections. Asked where the policy rate should sit at year-end, many participants judged it appropriate within or slightly below the current range, consistent with inflation fading on schedule. Many others judged it appropriate above the current range, and a few saw a case for raising rates at this very meeting, while still supporting the hold.1 The minutes describe this in words rather than a tally, but the direction is unmistakable: a meeting whose center of gravity has moved from when to ease toward whether to firm. For a Committee that spent the prior cycle debating the pace of cuts, a projection set with real weight on tightening is the defining signal of the meeting.

Divergent Views: The Case for Cuts

The confident read deserves its strongest challenge, and the minutes supply one. The benign case begins with energy. The de-escalation between the United States and Iran and the prospect of the Strait of Hormuz reopening have already pulled oil futures and near-term inflation compensation sharply lower, and the staff expected retail gasoline prices to fall and headline inflation to slow over the second half of the year.1 Strip the energy shock out and much of the acceleration reverses. The tariff contribution is a one-time step up in the price level, not a permanent rate of inflation, and the staff projected its effect to wane through next year, with inflation stepping down toward 2 percent by 2028.1 Housing services, a large component of core inflation, are still disinflating, and several participants expect that to continue.1 The productivity dividend from AI, once it arrives, expands supply and pushes costs down. And the tell that matters most for the doves is that longer-term inflation expectations have not moved from 2 percent, which means the un-anchoring the hawks fear remains hypothetical. On this reading, the June hold is the last stop before a cut, not the first sign of a hike.

The case is coherent, and it is why the Committee held rather than moved. It is not, however, where the balance of risk sits. The Committee itself judged the risks to inflation as skewed to the upside and the risks to employment as having moderated, and it deleted the easing bias rather than the tightening option.1 The benign scenario requires several things to break right at once: energy to stay calm, tariffs to pass through cleanly and fade, and AI-driven demand to cool on its own. The hawkish scenario requires only that current momentum persist. When one case needs a sequence of favorable resolutions and the other needs nothing new to happen, the second is the base case.

Implications

The consequences run in one direction. Rate-cut pricing now sits at odds with the Committee's own words, and the front end of the curve carries the asymmetry, its distribution of outcomes widened toward higher rates rather than lower. Over the intermeeting period the ten-year Treasury yield had already climbed about 20 basis points, and roughly 50 since the conflict began, while the two-year rose faster than comparable sovereign yields abroad as the market repriced the U.S. path higher.1 Duration bought on the assumption of imminent easing looks mispriced against a Committee that has deleted its easing bias and floated hikes. The dollar, already firmer as that rate gap widened, gains a further tailwind if the hawkish bloc grows.1 For anyone allocating capital, the operative assumption should be financing costs that stay elevated longer than the futures curve implied in the spring, with the squeeze falling hardest on small businesses and lower-credit households rather than on large corporates that can still issue freely.1 And because a majority favored shortening the statement and the Chairman opened a review of the Fed's framework, the communication regime is itself a moving variable: the words will carry more weight than usual precisely as they grow fewer.

The Verdict, and What Would Move It

The market that still prices the Fed's next move as a cut is reading the June meeting backward. The Committee held because the data left no cleaner option, then quietly removed the assumption that it was still heading down. The base case is a hold that runs longer than consensus expects, and for the first time this cycle the surprise the Committee is bracing for is a hike, not a cut.

The thesis confirms or breaks on a short list of variables. The first is the core PCE trajectory through the summer: a continued climb validates the hawkish bloc, a clean deceleration revives the case for holding into cuts. The second is energy and the Strait of Hormuz; the de-escalation that pulled oil and near-term inflation compensation lower is the assumption doing the most work in the benign scenario, and it is reversible. The third is the cadence of AI capital-expenditure announcements, the proxy for whether the demand impulse is intensifying or cresting. The fourth is any movement in longer-term inflation expectations, the tripwire that would force the Committee's hand. The last is the language of the shortened statement at the July 28 to 29 meeting, which will reveal whether the deleted easing bias was a pause or a turn.