Loading reports … Fetching the current index of long-form research.

Reports

Loading reports … Fetching the current index of long-form research.

The proposed Defense, Security and Resilience Bank shows how sovereign guarantees, capital markets, and industrial capacity are becoming the connective tissue of allied security.

Military power can be produced upstream of the battlefield, in factories, ports, shipyards, laboratories, mineral supply chains, skilled labor markets, and balance sheets. The battlefield only reveals what the upstream system was able to build in the years before the first shot.

For three decades, the allied world let that upstream system atrophy. Production lines were consolidated, inventories run down, suppliers offshored, and capacity tuned to the logic of peacetime efficiency rather than wartime endurance. Then Russia invaded Ukraine, and the bill for that efficiency came due. In allied wargames, forces frequently exhaust their stocks of precision munitions within days, and demand outstrips what the industrial base can supply.1

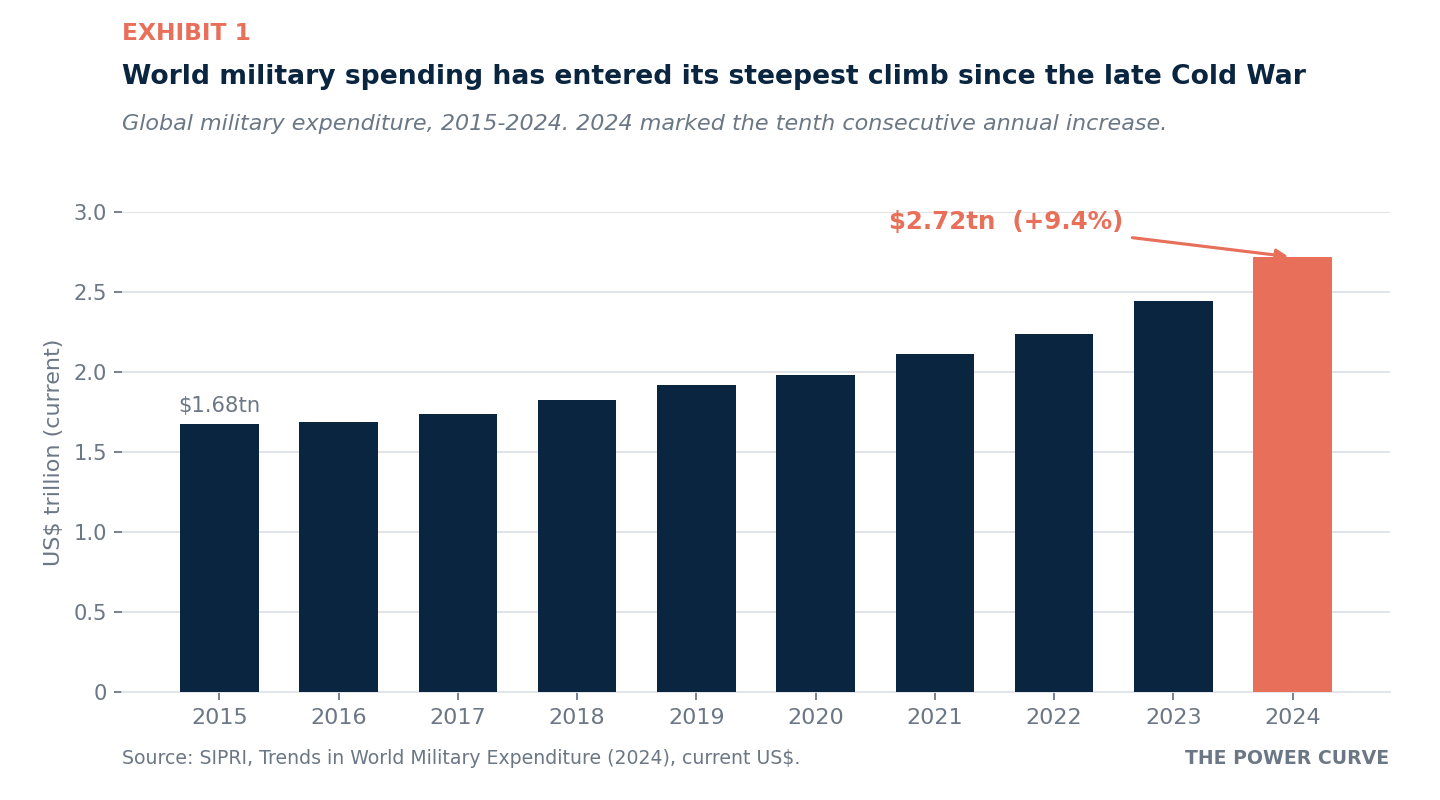

The political response has been to spend. At The Hague in June 2025, NATO members committed to invest 5% of GDP on defense and security by 2035 — 3.5% on core military requirements and a further 1.5% on resilience, infrastructure, and the industrial base.2 Global military expenditure reached $2.7 trillion in 2024, a 9.4% rise and the largest year-on-year increase SIPRI has recorded in nearly four decades.3

Money authorized is not capacity delivered. The proposed Defense, Security and Resilience Bank (DSRB) is the clearest institutional attempt yet to close that gap. And it points to something larger than itself: the conversion of defense finance into a standing strategic instrument.

The argument of this briefing is narrow. The DSRB is less about financing weapons than financing the capacity to make them. It reflects a shift in which capital markets, financial institutions, and manufacturing ecosystems have become instruments of deterrence. In an era of strategic competition, economic security depends on the ability to mobilize capital as quickly and credibly as military force.

The Defense, Security and Resilience Bank is a proposed multilateral lending institution — a financial institution backed by multiple sovereign governments — owned exclusively by nation-states and dedicated to financing defense, security, and resilience.4 It was conceived in 2025 by Rob Murray, a former head of innovation at NATO who designed the Alliance’s defense accelerator (DIANA) and its sovereign-backed venture fund, the NATO Innovation Fund.5 The proposal grew out of work developed inside the NATO International Staff and refined with multilateral-finance practitioners, and was given public form in an Atlantic Council report arguing that a dedicated defense bank could close allied funding gaps.6

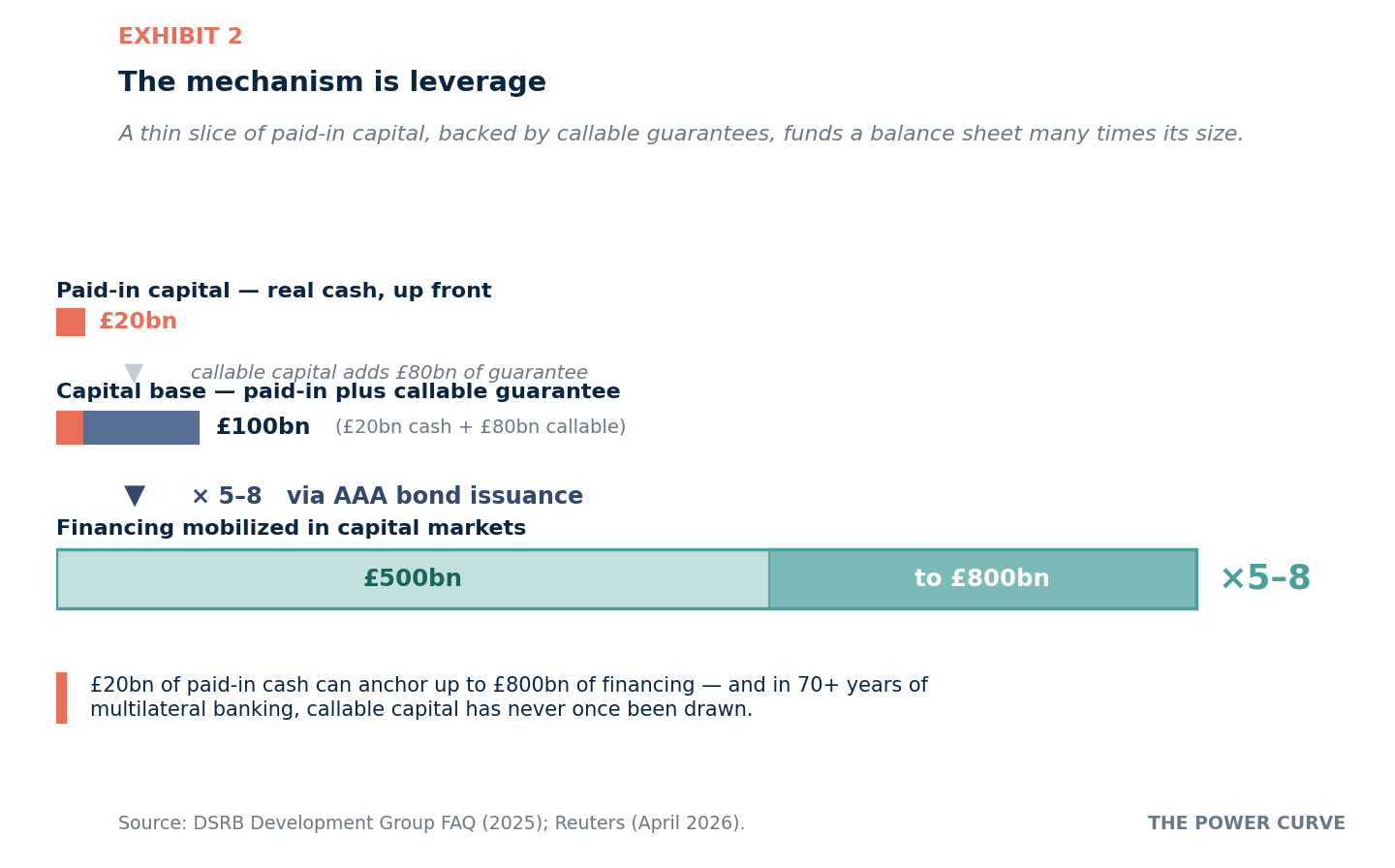

On the proposal’s design, the institution would follow the classic architecture of a multilateral development bank. Member states would contribute capital in two forms: paid-in capital, the real money provided upfront, set at roughly 20% of subscriptions; and callable capital, a contingent promise to provide more in a crisis, set at roughly 80%.4 Callable capital is what secures a top credit rating, because ratings agencies treat it as equivalent to strong sovereign backing. In more than seventy years of multilateral banking, callable capital has never been drawn. On the working design, an initial balance sheet of about £100 billion (roughly $135 billion) — £20 billion paid in, the remainder callable — would let the bank multiply each unit of sovereign capital into five to eight units of financing through bond issuance, targeting a AAA rating.7

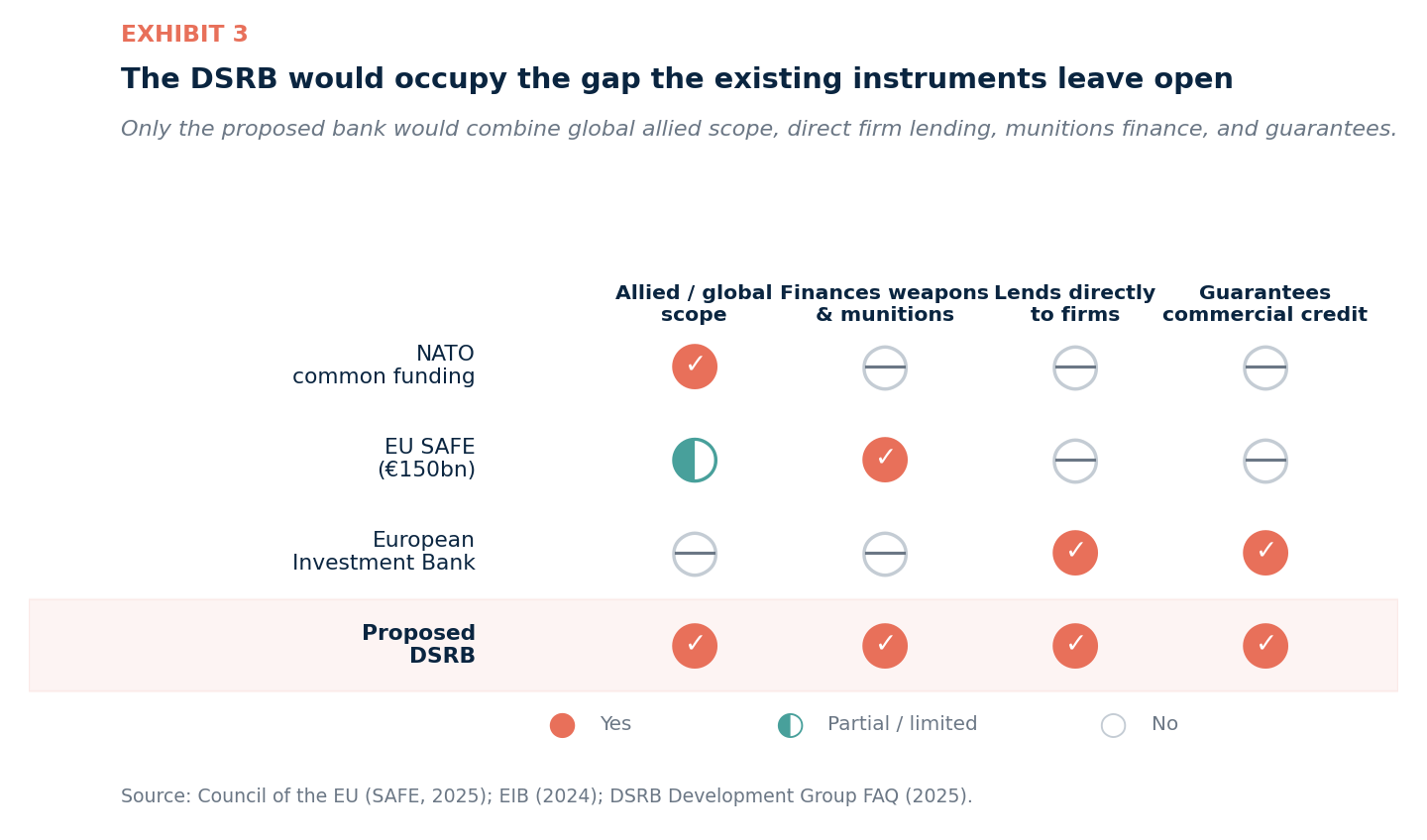

What it would finance separates it from everything that exists. The DSRB is designed to lend to sovereigns for national defense and resilience projects; to lend directly to companies — primes, SMEs, and tier-two and tier-three suppliers — that hold government contracts; and, most consequentially, to guarantee commercial-bank lending to the defense supply chain, reducing the risk weightings that constrain banks under the incoming Basel IV capital rules.4 That guarantee-and-risk-sharing function is what would separate the institution from a conventional sovereign loan book. Eligible projects would span munitions, drones, and maritime autonomy; resilient infrastructure such as military mobility, energy, and logistics; and dual-use technologies including artificial intelligence and space.4

The proposal has advanced from concept toward agreement. The DSRB Development Group — a temporary, not-for-profit entity created to convene nations and prepare charter negotiations — gathered representatives from 37 nations, including every G7 member, alongside the European Commission, NATO, the European Parliament, global banks, and ratings agencies in the City of London in September 2025.8 Multilateral negotiations on the bank’s charter concluded in Montréal in April 2026. On 29 April 2026, nineteen founding member nations selected Canada as the future host of the bank’s headquarters, subject to ratification.9 Canada — whose Business Development Bank chief executive, Isabelle Hudon, served as lead negotiator — emerged from the founding wave as the institution’s anchor state.10

Precision about status matters here, because the design is settled further than the institution is. The charter has been negotiated but not ratified; ratification requires legislative approval by the founding governments, expected to take months rather than weeks.7 No capital has been subscribed. No bond has been issued. No loan has been made. Major commercial institutions, including Deutsche Bank, have publicly backed the concept.11 But backing is not subscription, and an agreement is not an operational bank. The DSRB today sits between negotiation and capitalization — further than skeptics expected a year ago, and not yet a lender.

The prior question is why defense needs a bank at all. Governments are sovereign borrowers. They can issue debt directly. Why route the problem through a new institution?

Because higher defense spending does not convert automatically into military capacity. Defense production has long lead times, specialized suppliers, security restrictions on who may build what, and — until recently — uncertain demand. A facility to forge artillery barrels or fill shells is a capital-intensive, multi-year commitment. No firm builds it on the strength of a single year’s budget line that may not be renewed.1

This is the structural trap. Governments fund defense in annual cycles bounded by fiscal rules; industry requires multi-year, predictable financing to expand capacity. The two clocks do not align. A supplier asked to triple output needs certainty stretching over a decade; a defense ministry can rarely promise beyond the next budget.

The friction is sharpest at the bottom of the supply chain. Small and medium-sized enterprises — the specialist machine shops, component makers, and sub-tier suppliers on which primes depend — face higher costs of capital and thinner balance sheets. The cost of capital is the return that lenders and investors require to finance an investment; the higher it is, the harder long-duration industrial expansion becomes. For a small supplier, a single defense contract can pose an existential concentration risk, and commercial lenders price it accordingly. These are ordinary capital-market frictions — information gaps, concentration risk, illiquidity — operating on a sector where the social return far exceeds the private one.

Three further forces have narrowed commercial finance. Environmental, social, and governance mandates pushed some institutional investors away from the sector. Reputational caution and legal restrictions thinned the pool of lenders. And the incoming Basel IV banking framework raises the capital that commercial banks must hold against concentrated, capital-intensive exposures — tightening credit to defense suppliers as demand surges.4

Existing public institutions cannot fully close the gap. The European Investment Bank has expanded its security lending and dropped the dual-use requirement for military equipment, but it still cannot finance weapons and ammunition.12 The European Union’s SAFE instrument offers €150 billion in long-maturity loans, but only to governments, only within a European framework, and without the guarantees that pull in private capital.13 Each is real. Neither is a defense bank. Whether a dedicated bank is the right answer to Europe’s rearmament financing dilemma is itself contested.14

Here is the frame that organizes the rest. Beneath the visible architecture of deterrence — the missiles, the brigades, the carriers — sits a less visible layer that determines whether any of it can be built and sustained. Call it the capital layer of deterrence.

Deterrence is the ability to discourage an adversary from acting by making the expected costs of acting exceed the expected benefits. It rests not only on fielded forces but on the credible prospect of sustained production — the adversary’s belief that you can out-build and out-last them. That belief is manufactured upstream, in capital markets, long before it is tested downstream.

The DSRB is designed to convert political commitments into investable capital. The chain runs as follows.

Each link converts political will into deterrent effect, and each can fail.

| Layer | Function | Strategic question |

|---|---|---|

| Political commitment | Governments pledge to spend and to stand behind the institution | Is the pledge credible and durable? |

| Sovereign backing | Paid-in and callable capital give the bank a balance sheet | Will enough states subscribe enough capital? |

| Institutional finance | A AAA-rated bank borrows cheaply in markets | Can it earn and hold the top rating? |

| Lower cost of capital | Cheap, long-dated funding reaches industry | Does the saving reach suppliers, not just primes? |

| Industrial investment | Firms build plant, tooling, and inventory | Is demand credible enough to justify the build? |

| Production capacity | Output of munitions, platforms, and components rises | Does capacity expand or merely consolidate? |

| Military capability | Forces are equipped and resupplied at scale | Does capacity become fielded readiness? |

| Deterrence effect | Adversaries revise their cost-benefit calculus | Does the adversary believe it? |

Each link is a point of leverage and a point of failure. A pledge that markets doubt produces no rating advantage. A high rating that does not lower the cost of capital for sub-tier suppliers produces no new capacity. Capacity that never reaches the field produces no deterrence. The chain is only as strong as its weakest conversion.

What the design attempts is to industrialize this conversion — to take the diffuse, episodic, politically contingent promise of allied defense spending and turn it into a standing mechanism that prices and funds capacity at scale. The strategic insight is that credibility itself becomes collateral. Pooled sovereign backing is more creditworthy than most individual members; the bank would monetize that pooled credibility and lend it forward to the firms that build deterrence.

This is why the institution is better understood as financial infrastructure for deterrence than as a procurement vehicle. It would not buy weapons. It would build the capital layer required to make the arsenal feasible to build.

Strategic transitions generate financial institutions. The regularity is strong enough to treat as evidence rather than analogy.

The Bretton Woods conference of 1944 produced the International Bank for Reconstruction and Development — the World Bank — to finance postwar reconstruction when private capital would not flow to devastated economies on acceptable terms. The Marshall Plan channeled roughly $13 billion into European recovery between 1948 and 1952, rebuilding industrial capacity as a bulwark against Soviet expansion. The European Investment Bank was created by the Treaty of Rome in 1958 to finance European integration. After the Cold War, the European Bank for Reconstruction and Development was founded in 1991 to finance the transition of former Communist economies to market economies. Export credit agencies and development finance institutions have played a quieter version of the same role for decades, underwriting strategically important trade and investment that commercial lenders found too risky.

Each was built to meet a strategic shock that private markets, acting alone, would underprice or ignore. Each used sovereign backing to attract private capital toward an objective with security value beyond private returns.

The claim is not that the DSRB resembles these institutions in form. It is that the allied world has repeatedly answered a structural strategic shift by building new financial machinery — and that the present moment, defined by industrial under-capacity against a rearming Russia and a manufacturing-dominant China, fits the pattern. The novelty is the target: where earlier institutions financed reconstruction or transition, this one would finance deterrence itself.

Strategic eras build financial machinery; the DSRB’s test is conversion into capacity.

| Institution | Strategic context | Financial mechanism | What it financed | Lesson for the DSRB |

|---|---|---|---|---|

| World Bank (1944) | Postwar reconstruction | Paid-in plus callable capital; AAA bonds | Reconstruction and development lending | Callable capital and a top rating can mobilize vast private funding |

| Marshall Plan (1948–52) | Containment of Soviet influence | Direct sovereign grants (~$13bn) | European industrial recovery | Rebuilding industrial capacity is itself a security act |

| European Investment Bank (1958) | European integration | Sovereign-owned bank; market borrowing | Infrastructure and cohesion; limited defense | Mandates bind — the EIB still cannot fund weapons |

| EBRD (1991) | Post-Cold War transition | Sovereign-owned; conditional lending | Market and institutional transformation | A bank can pursue strategic, not only commercial, ends |

| Export credit / DFIs | Strategic trade and investment | Sovereign guarantees and risk-sharing | Politically important exports and projects | Guarantees draw private lenders to risky strategic ends |

| Proposed DSRB | Allied rearmament; industrial under-capacity | Paid-in plus callable capital; guarantees; AAA bonds | Defense supply chains, SMEs, dual-use, resilience | Unproven: whether finance converts into delivered capacity |

Those institutions endured because they solved recurring market failures. The DSRB confronts the same family of failures, and naming them clarifies both the promise and the danger.

Deterrence is a public good. Its benefits are shared across an alliance and cannot be captured by any single firm or nation. No private actor will fund standby production capacity at the socially optimal level, because the security returns accrue to everyone and the financial returns to almost no one. This is the textbook case for public intervention — and the strongest argument for the bank.

The sharper problem is a coordination failure. Suppliers will not invest in capacity without credible, durable demand; governments cannot generate capacity without suppliers investing first. Each waits for the other. A multilateral lender offering multi-year financing and offtake-style certainty could break the standoff by making the demand signal credible enough to act on, smoothing the boom-bust cycle that has long plagued procurement.

Beneath both lies the logic of strategic externalities. Industrial capacity carries security value far beyond its private profit. A live artillery-shell line is worth more to an alliance than its balance sheet suggests, because its option value in a crisis is enormous. Markets do not price option value for deterrence. Sovereign-backed finance can.

The mechanism that does the work is the sovereign guarantee, applied through risk pooling. By combining the credit of many sovereigns, the bank would convert dispersed, individually weaker balance sheets into a single stronger one, and lend that strength forward. Callable capital and government backing would turn a risky, concentrated, politically exposed sector into one that markets fund at low cost — and, by sharing risk with commercial banks, the bank could crowd in private capital that would otherwise stay on the sidelines. Public finance here is not a substitute for private capital but a catalyst for it.

The dangers mirror the design. Cheap, sovereign-backed capital is precisely the kind that funds weak projects when governance is poor — the classic moral hazard of subsidized credit. A lender operating in a politically charged sector invites political allocation: loans steered to national champions or favored constituencies rather than to the projects that most expand capacity. And the same callable capital that secures the rating concentrates contingent liability on the largest members, who will expect commensurate control. Weighted voting, safeguards against bloc dominance, and disciplined project selection are therefore not administrative detail. They are the difference between an instrument of deterrence and a subsidy machine.

For the DSRB to matter, several conditions must hold at once.

It needs sufficient sovereign membership and real capital commitments — not expressions of interest, but ratified subscriptions large enough to give the balance sheet weight. It needs governance credible enough to resist political allocation while remaining accountable to shareholders. It needs a clear mandate and the discipline to select projects that expand productive capacity rather than reward incumbency.

It must coordinate, not collide, with the institutional field already in place: NATO’s capability targets, the European Union’s SAFE instrument and its European Defense Industrial Strategy,15 national defense ministries, export credit agencies, and the commercial banks it intends to de-risk. Duplication is the most immediate practical risk. The proposal’s own answer — that it would complement SAFE (which lends only to EU governments) and the EIB (which cannot fund weapons) by lending across the full allied perimeter and directly to firms — is plausible, but it must be demonstrated, not asserted.4

It must reach the bottom of the supply chain. If cheap capital flows only to prime contractors with strong balance sheets, little changes; the binding constraint is the under-capitalized SME tier. And it must handle the politics of dual-use and lethal systems transparently, so that financing munitions does not become a liability for legitimacy.

The whole edifice rests on earning and holding a top rating. The AAA target is credible on the standard multilateral template, but it is contingent on conservative leverage, robust risk controls, and the market’s confidence that callable capital is genuinely callable. Lose the rating, and the cost-of-capital advantage that justifies the institution disappears.

A sober assessment must take the strongest objections seriously.

The first is duplication. Europe already has the EIB, SAFE, the European Defense Industrial Strategy, and national mechanisms. A new bank risks adding institutional layering and overhead without adding net capacity. The DSRB’s global, allied scope and its company-level lending are genuine differentiators — but governance overlap and turf competition are real.

The second is speed. Multilateral banks are deliberate institutions. Charters must be ratified, capital subscribed, ratings earned, and lending operations stood up — a process measured in years. The capacity shortfall is measured in months. The bank could arrive credible but late.

The third is governance capture. Lending into a politically sensitive sector, across nineteen or more sovereign shareholders with divergent industrial interests, invites contested allocation. Weighted voting concentrates influence; safeguards can erode.

The fourth is incumbency. The easiest loans to make are to the largest, most bankable firms. A bank under pressure to deploy capital may subsidize consolidation among primes rather than finance new entrants and expanded capacity — the opposite of its stated purpose.

The fifth is legitimacy. ESG constraints, public discomfort with financing lethal systems, and legal complexity around sovereign immunity and cross-border enforcement could each slow or narrow the institution.

The deepest objection is the most important: financing is necessary but not sufficient. Capital does not by itself fix slow procurement, permitting bottlenecks, shortages of skilled labor, constrained munitions inputs such as energetics and machine tools, or the absence of long-term demand signals. A bank can lower the cost of building capacity. It cannot, alone, build it. If procurement reform, workforce, permitting, and offtake do not move in concert, cheaper capital will simply chase the same constraints.

The binding risk is not finance but everything finance cannot fix.

| Risk | Why it matters | Mitigation |

|---|---|---|

| Duplication of existing institutions | Wastes resources, adds overhead, blurs accountability | Sharp mandate boundaries; explicit complementarity with SAFE, EIB, NATO |

| Too slow for urgent need | Capacity gap is immediate; banks are deliberate | Phase in via guarantees and co-financing before full lending |

| Governance capture | Politicized lending erodes credit quality and trust | Independent management; safeguards against bloc dominance; transparency |

| Subsidizing incumbents | Funds consolidation, not new capacity | Mandate to reach SMEs and tier-2/3 suppliers; capacity-linked criteria |

| Legitimacy and ESG | Financing lethal systems invites legal and public friction | Clear dual-use rules; sanctions compliance; disclosure |

| Finance without the rest | Capital cannot fix procurement, labor, inputs | Pair lending with procurement and industrial-policy reform |

If it succeeds, the DSRB would reshape incentives across the strategic landscape.

For NATO, it would supply the financial guarantees that underwrite its security guarantees — converting the 5% spending pledge into a mechanism that funds industrial expansion rather than merely scores it.2 For Europe, it would complement SAFE and the EIB by reaching beyond the EU perimeter and lending to firms, not only states. For Canada, hosting the headquarters is a positioning move, anchoring a new multilateral institution on its soil and tying its rearmament to allied capital.9

For the United States, the bank offers a way to mobilize allied balance sheets toward shared industrial capacity, and to insulate part of allied defense financing from the volatility of any single national budget cycle. For Ukraine, a standing mechanism to finance defense supply chains across the alliance is ultimately a means to sustain the arsenal it depends on.

For Russia and China, the signal is the point. Both have shown that industrial mass and the ability to sustain production are themselves instruments of coercion. An institution that credibly lowers the cost and raises the speed of Western capacity expansion would alter their calculus about what a long confrontation would cost them. That is deterrence operating through the capital layer.

For private capital and defense suppliers, the bank would reprice the sector. Guarantees and risk-sharing would pull commercial lenders back toward an industry they had been leaving, and offer SMEs a path to the long-dated financing they have never reliably had.

The largest implication is conceptual. The DSRB is one expression of a shift from military alliances to industrial alliances — from pooling forces to pooling the financial and manufacturing capacity that produces forces. Economic security and military security are converging into a single problem, and the institutions built to address it are starting to look as much like banks as they do armies.

The DSRB would not be the arsenal. It would be part of the machinery that lets the arsenal exist — the capital layer beneath the visible architecture of deterrence.

That is why it matters, and why it must be judged strictly. The proposal has moved further than skepticism allowed: a negotiated charter, nineteen founding members, a host country chosen, commercial banks at the table. It has also not been ratified, capitalized, rated, or made a single loan, and it has not yet demonstrated that pooled sovereign credibility can translate into capacity at the bottom of the supply chain, where the constraint actually binds. The United Kingdom — whose national conceived the idea — has so far declined to join, preferring a separate European mechanism, a reminder that allied alignment here is real but incomplete.16

This is the change in the model the DSRB forces. For most of the postwar period, allied security was measured in what was spent and what was fielded. The contest now reaches one layer deeper, into the institutions that can turn sovereign credibility into productive capacity — quickly, at scale, and for long enough to change an adversary's beliefs. That capacity does not yet sit in any bank’s vaults. It exists, for now, only in a charter awaiting ratification and in governments' willingness to stand behind it.

Whether allied states convert that willingness into subscribed capital is the open question. The competition of this century will be settled less by what is spent than by what can be built — and by who builds the machinery to finance the building.